THE WEEKEND REPORT (Formally, "The Weekly Top 10")

THE WEEKEND REPORT

Table of Contents:

1) With liquidity being drained (more aggressively), multiple compression will cause markets to fall further.

2) This is not a normal tightening cycle. The Fed is fighting more than just inflation!

3) A few candidates for those who will be expose as “swimming naked” in the months ahead.

4) The dollar has become ripe for a short-term (but still a multi-week) pullback.

5) A bullish development on the technical side of things last week for the S&P 500 Index.

6) However, the MACD charts on the SPX, NDX, & SMH point to some further problems ahead.

7) Crude oil saw a negative MACD cross and a death cross last week….Ouch.

8) The best house in a lousy neighborhood can still be a tough place to live.

9) Lower gasoline prices have bolstered the Democrats with two months to go until the midterm elections.

10) Summary of our current stance……The markets and economy are still “out of balance.”

1) Many investors are bottom-up investors, while some investors start from a top-down outlook. In our opinion, they are both incredibly important. HOWEVER, they’re both a bit less important than they usually are today. In our opinion, these macro & micro issues will merely tell us how low the market will fall and how far many stocks will decline…not WHETHER they will fall or not. Given that liquidity is going from a massive injection to a significant removal, the market is likely headed lower as the markets adjust to the change in valuation levels that needs to take place now that the Fed is removing liquidity from the system.

Many of the great long-term investors spend a lot more time looking at individual companies and their stocks in a bottom-up fashion. They care much more about the revenues, earnings, costs, etc. of a company…than what’s going on in the big picture in the economy. However, even the most ardent bottom-up investor also likes to look at the macro landscape…so that they can have a good idea about how those developments will impact the micro issues for the companies they’re considering. .

Right now, however, we strongly believe both macro and micro issues will take a very slight back seat to the issue of valuation…given the ENOURMOUS shift in liquidity flow that is taking place this year in the financial system. These macro and micro issues will certainly play an important role as to HOW FAR the stock market will decline during the process of “deliquidation”…and have an impact on when specific stocks will bottom…but they will not play as big of a role as they usually do in determining whether the market will rise or fall further over the coming months. (BTW, we don’t think “deliquidation” is an actual word, but since “reliquidation” IS a word, we’re going to run with it! 😊)

We (strongly) believe that too many people still believe that if we can see a “soft landing” or avoid a recession, the stock market will stabilize and rally back to new highs. We think that this is all but impossible. No, we’re not saying that a soft landing is impossible. We’re saying that even if we get one, the stock market still has further to decline. (That said, we do thing a soft landing is quite unlikely.) In our opinion, It will take a huge bounce in economic growth to achieve a significant rally from current level…not to mention a new all time high. Merely avoiding a recession will not be anywhere near enough to help the market rally back to above its old highs.

The simple reason for our thinking is that the stock market…and other markets…were pushed to valuation levels that they could never reach on their own…and they will have to come down to much lower levels before they can stabilize on their own. It was the massive liquidity programs that was instituted to save the global economy and the global financial system that took them to such heights. Now that this liquidity is going to be removed in a much more meaningful fashion (QT), we’re going to have to see more realistic levels going forward.

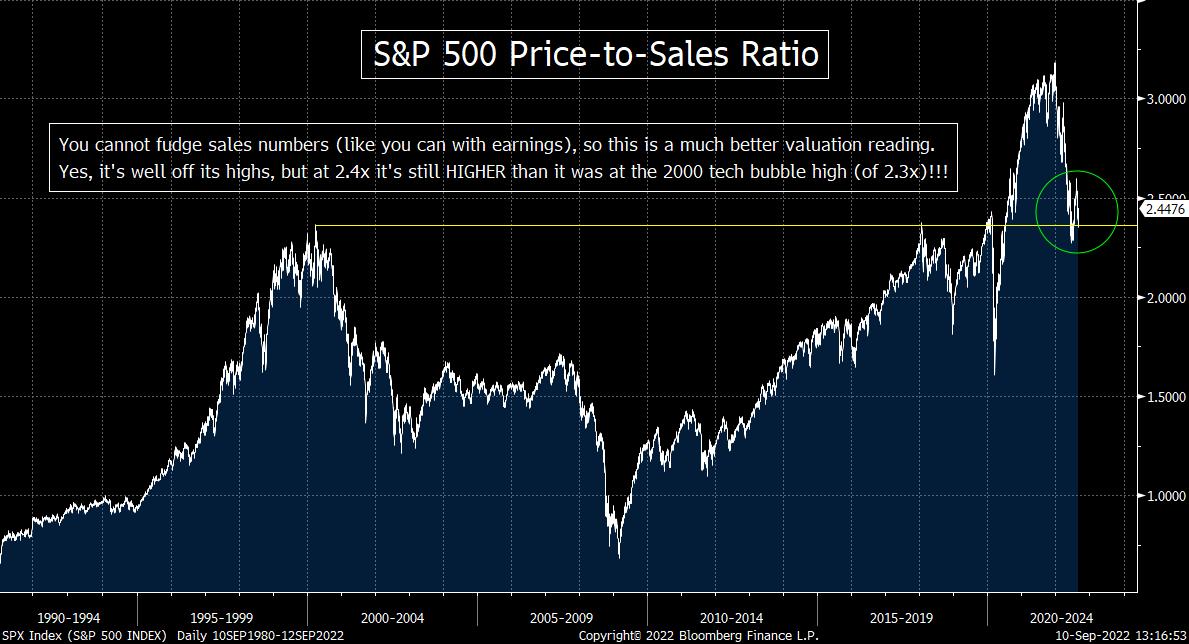

We’re not just talking about P/E ratios either. If you look at the price-to sales ratio, it’s STILL higher than it was at the tech bubble HIGH of early 2000!!! Thus, it’s not even in the same area code as the historic average price-to-sales ratio!!!.....Also, at over 4x, the price-to-book value for the S&P 500 is miles away from anything that he market has seen outside of the tech bubble of the late 1990s (that was fueled by excess liquidity during the Y2K problem) and the recent liquidity fueled rally during the pandemic.

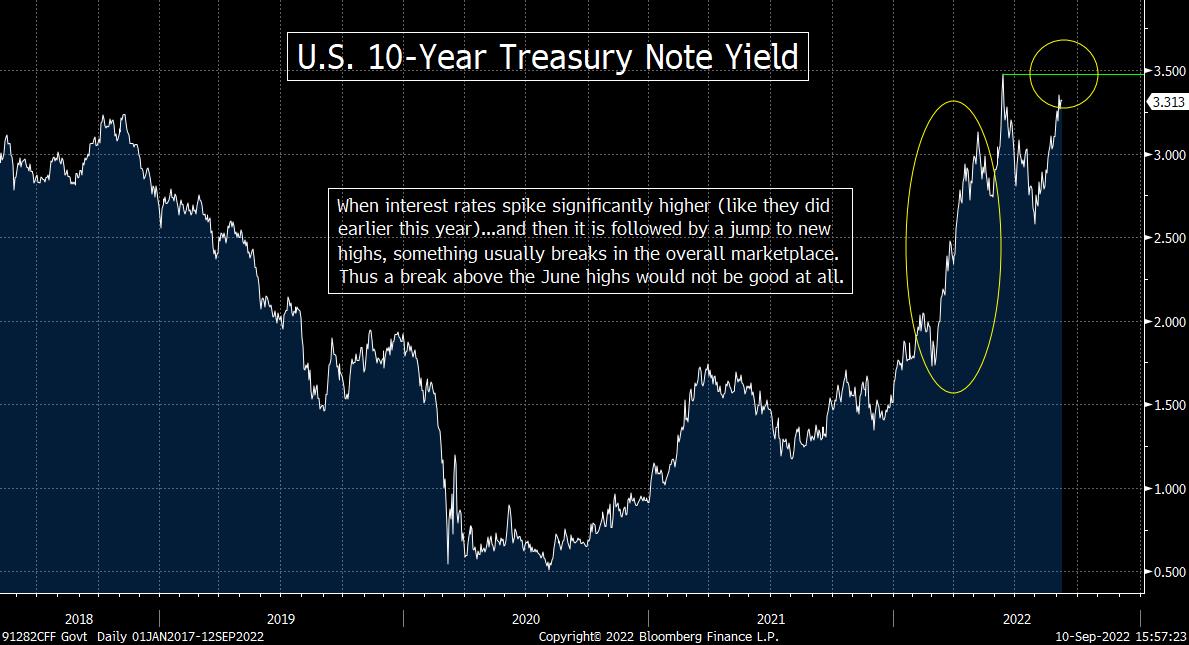

Many pundits will say the low level of interest rates that exist today will justify 20x earning. Well, first of all, the yield on the 10yr Treasury note is up almost 600% since the 2020 lows. Besides, if low yields justified excessively high valuations, why haven’t we seen high valuations in Japan over the past 30 years…and why didn’t we have them during the 1950s when rates were so low? More importantly, history shows that the only time we’ve had a multiple above 20 was during the two periods when massive liquidity was pushed into the marketplace. (In the late 1990s…to help the system during the Y2K problem…and 2020-2021 during the pandemic.)

Therefore, with the Fed removing the liquidity their massive liquidity…the steroids that pushed valuations to extreme levels…we’re going to have to see the kind of multiple compression that will move it back in line with historical averages. For us, you have to take out the periods of hyper-liquidity when calculating the average multiple…because they were artificially induced. No, we did not takeout ALL of the times when valuation levels became extended…because most of those times, it was over-enthusiastic investors that drove them to 17x or 18x earnings, not artificial stimulus (at least not in a significant way). The same is true when the market reached undervalued levels…when panicked investors took them to ultra-low levels. Thus, we don’t remove those low number because they were reached by the natural movements in the stock market.

When you remove the two non-steroid induced eras of the last 1990s and 2020/21, the average P/E ratio is closer to 15.5x earnings. Since every bear market since WWII has not bottomed until the pendulum swung to an undervalued level (14.5x is the average), the decline will almost certainly have to be bigger.

In other words, this was always going to happen when the Fed reversed its policy. Valuation levels are driven by liquidity…and liquidity is becoming less plentiful. For the stock market to reach its natural level, it’s going to have to decline further…likely quite a bit further. Therefore, we can spend a lot of time on how much the economy is going to shrink going forward all we want. We can also spend a lot of time trying to figure out what companies will earn going forward. However, without the massive liquidity that the Fed was providing in 2020 and 2021, investors are not going to pay the same level for those earnings…..With all of this in mind, we believe investors should remain defensive as we move through the rest of 2022.

2) We believe that too many people don’t realize that this tightening cycle had to become a tougher, more prolonged one once Russia invaded Ukraine. The Fed is not just fighting inflation! They’re also trying to push the markets back into equilibrium with their underlying fundamentals. They were always going to tighten their emergency policies…whether inflation became a problem or not. When it DID become a BIG problem, this process pretty much HAD to become a more painful one than most people recognize.

We want to take what we said in the first bullet point to another level. What we reviewed in that first point is one of the themes we’ve been pushing for several weeks (even months) now. We believe that too many pundits are trying to analyze today’s situation with the thought that the stock market was trading at (or close to) a level that could have been justified by the underlying fundamentals back at the end of last year…..Therefore, they are arguing that now that we’ve already seen a 20% decline in the stock market, it is correctly reflecting the economic weakness that has already taken place this year…and that will likely take place in the future. This, in our opinion, is the wrong way to analyze today’s situation.

We can spend a lot of time talking about whether inflation will be come enough for the Fed to stop raising interest rates all we want. However, we have to realize that the real goal for the Fed is to take interest rates back to a level that they deserve to be standing on their own…without massive central bank intervention. Too many pundits seem to have forgotten that interest rates stood at artificially low levels in 2020 and 2021 (and thus the stock market stood at an artificially high level). Therefore, we think they are making a mistake when that believe that it will merely take a “normal” tightening cycle to move the system back into equilibrium.

Inflation has become a much bigger problem…due to the Russia invasion of Ukraine…than it would have been if had only been pushed somewhat higher by the big QE and big fiscal programs of the past few years. However, the Fed was always going to have to tighten more than they would normally tighten because they’re not just fighting inflation!!!!!!! They’re ALSO trying to push the markets (not just short-term interest rates) back into balance (equilibrium) with their underlying fundamentals!

Another big problem that we don’t believe that enough people are thinking about is that the removal of such massive levels of liquidity was always going to hurt the economy more than a normal tightening cycle would do. The much lower levels of liquidity sloshing around the system is also going to have an outsized impact on the amount of money private equity firms and venture capital firms have at their disposal to invest in new companies. In other words, this tightening cycle is not just going to involve higher interest rates that will raise the cost of investing in businesses…there will also be a lot less money available to invest in those businesses! Therefore, the negative impact this tightening cycle has had…and will have…on the economy will be more pronounced than usual.

In other words, a usual tightening cycle merely involves just the raising of interest rates. This one, however, also includes the tapering back of a massive QE program…and the institution of a significant QT program. The Fed was always going to have to tighten policy EVEN if inflation had not become a problem. Therefore, the fact that inflation DID become a BIG problem…meant that this tightening program was always going to be a tough one…and a much longer and more pronounced one that most pundits seem to understand. Therefore, they don’t realize that the Fed will keep on tightening…even if inflation falls in a material way going forward. Sure, they’ll find something…somewhere…to claim that they’re tightening further because of continued inflation pressures. However, the real reason will be that they want to keep their tightening policy in place…at least to some degree…until the markets and the economy move back into balance with one another……This, in our opinion, is why they’re using the word “pain” more often in their rhetoric now-a-days.

3 Last weekend, we highlighted that it’s during the second leg of a bear market that “naked swimmers” get exposed…and the REAL start to have a much bigger impact on the stock market. These “naked swimmers” could show up in anywhere, but we have a few candidates for where they might raise their ugly heads.

Last weekend, we spent a lot of time talking about how it’s the second leg of a bear market (not the first leg) that exposes the “naked swimmers”…and THAT’S when thing get really ugly. This week, we wanted to offer a few potential candidates that might become the “naked swimmers” that are exposed this time around…the way WorldCom, Enron, Bernie Madoff, etc. were exposed in previous bear markets. (Not all of those who are “exposed” are cheats. Many of them are very honest businesses or people…who merely got in over their heads…or took on too much leverage.)

One situation that stands out to us is the cryptocurrency market. Last week, Poolin…one of the largest providers of Bitcoin mining-pool services…halted withdrawals yesterday in an effort to preserve liquidity didn’t get more attention! Remember what happened the last time we saw these kinds of restrictive developments in the crypto market? It was followed shortly thereafter by some serious “forced selling” in that asset class. That, in turn, caused some serious selling in the stock market…because the crypto market was not liquid enough for the leveraged investors in that market to raise the money they needed to meet their margin calls. Therefore, they sold what they could…which was mostly big cap tech names. (Crypto holders don’t own GE, GM and MMM!)

Of course, a lot of leverage was wrung out of the crypto market in the spring, so maybe the renewed decline in Bitcoin and other cryptos will not create the same kind of pressure on the stock market as it did in the spring. However, it is still a key “risk-on/risk-off” asset, so if it

continues to decline in the coming days and weeks, it will not be good for other risk assets…..Bitcoin did bounce strongly on Friday, so it still trading above its summer lows. However, if it breaks below those June lows at some point in the near future, it could signal some big problems in other risk assets as well.

Another issue is one that we admit is a rather vague one, but it’s still something that concerns us. We have seen an ENOURMOUS jump in corporate debt over the past dozen years…and especially in the last 2.5 years. U.S. companies now have almost $11 trillion in outstanding debt securities today. Total U.S. corporate debt (both non-financial and financial corporations) is over $22.5 trillion…almost twice what it was with global in 2007-08. Finally, global corporate debt is more than $86 trillion dollars today!

The Fed’s monthly QT program is set to double this month. Of course, the bonds they buy are Treasury and MBS bonds, not corporate debt. However, corporate debt is priced off of Treasury debt, so any move in Treasury prices (and thus Treasury yields) can and do have a big impact on corporate bond prices. Former Fed trader , Joseph Wang, said in this week’s Barron’s that the CBO is looking for a trillion dollars a year of issuance of Treasury securities for the foreseeable future…vs. a net supply of $500 billion before Covid. With QT coming into play, that will make the issuance $1.5 trillion…with the marginal buyer (the Fed) no longer scooping up those securities…..With all of this in mind, it’s hard to think that Treasury yields (and thus corporate bond yields) will not rise further…which could create another blow up in the credit markets in the months ahead.

Finally, we have the energy markets in Europe. Last week, we read that the European energy trading markets were in turmoil. One article touched on the idea that those European energy markets could actually halt…unless European governments extended liquidity to cover margin calls of at least $1.5 trillion. (This, according to the Norwegian energy company, Equinor ASA.) No, we’re not talking about the proposals that would give individuals money to curb their energy costs. We’re talking about energy traders! What if a serious problem with counter party risk were to develop…and people stop trading with one or more entities? That could create problems in the physical delivery market as well………As we learned during the GFC, whenever the problem of “counter party risk” raises its ugly head, it’s always bad for risk assets.

Okay, let’s step back for a moment. We are NOT saying that any of these issues will be coming to a head soon. (The last thing we want to do is to start rumors about troubles with European energy traders. We’re just highlighting that there are reports out Europe that are concerning to us.)….Also, the situation in the cryptocurrency market and the corporate bond market might not become big problems going forward. We just want to highlight that there ARE some warning signals that coming to light right now…and since the second leg of bear markets tend to expose “those who are swimming naked” (to steal a phrase from Warren Buffett)…we wanted to suggest these areas in the marketplace to keep an eye on going forward. If the cracks in these markets begin to widen, it would send up a major warning flag for investors in many different risk asset markets.

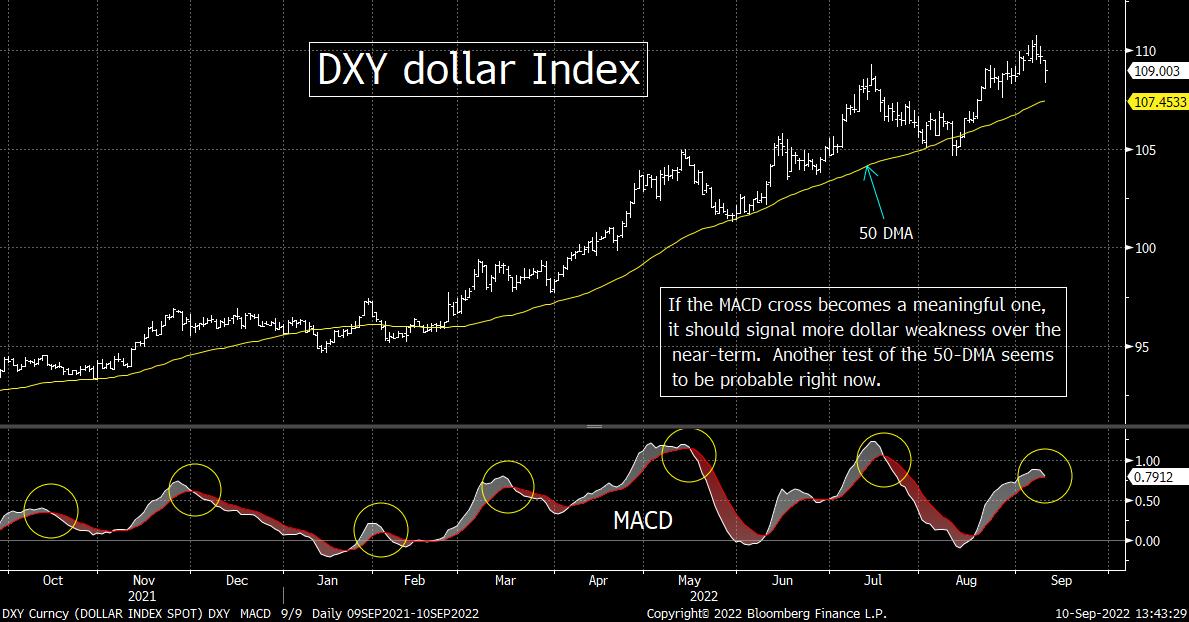

4) By the beginning of last week, the dollar had become quite overbought on a technical basis…and extremely over-loved in terms of sentiment. Therefore, it had become ripe for a pullback. Looking at last week’s action…and its impact on the MACD chart on the DXY dollar index…we should be looking at a decline in the dollar that will last for at least a couple of weeks.

One of the strongest trends in the marketplace we’ve seen this year has been the strength in the U.S. dollar. In fact, this rally has been something that began in earnest in June of 2021 (after the DXY dollar index made a nice “double-bottom”…and very close to the time that the Fed started talking about “tapering” in a meaningful way). However, like all “trends,” the 15-month rally in the dollar has not come in a straight line. It has seen several pullbacks along the way. Right now, we seem to be moving into one of those multi-week periods were the U.S. dollar does indeed retreat for a while.

The reason we say this is because, earlier this week, the DXY dollar index had become quite overbought its RSI chart. When that has taken place in the last year, the dollar has seen a short-term pullback. Similarly, its MACD chart is now very close to a negative cross…and whenever it has seen a meaningful negative cross on its MACD cross over the past 12-15 months, it has been followed by a decline in the greenback that has lasted for at least a week or two……….Finally, bullishness in the dollar had become extremely high…with bullishness among futures traders in the DSI data reaching 93% early this week!

No, this does not mean that the dollar is going to roll-over in a major way over many months, but it should be telling us that we’ll see more weakness over the near-term. This, in turn, could be something that could/should help the stock market…especially since it is coming off an oversold and over-hated hated.

HOWEVER, as much as a weaker dollar could help the stock market on a very-short-term basis, we question how much it will help it for more than a few days. As we just highlighted, some dollar weakness could help sentiment in the stock market over the very-short-term, BUT history tells us that the correlation between the stock market and the dollar is a VERY mixed one….Yes, there have been several times when the stock market has moved in the opposite direction as the dollar, but there have also been many times when they’ve both moved in the same direction in tandem. For instance, they moved in opposite directions in 2020 after the Fed enacted its huge QE program…and the same took place in 2017. However, the stock market and the dollar moved in the same direction together in 2014, 2016 and 2019…just to highlight a few examples.

In other words, we think it’s going to be hard for the stock market to see a sustained rally…even if the dollar continues to fall over the coming days and weeks. This is especially true since the decline in the dollar will very likely be just a technical one…and thus probably won’t be an extended one. Therefore, it will not be long enough to signal that the Fed is going to pivot soon…and start cutting rates………We’re merely saying that the dollar is very likely headed lower over the short-term…and thus currency traders will need to be careful about their somewhat crowded bullish bets on the greenback over the near-term.

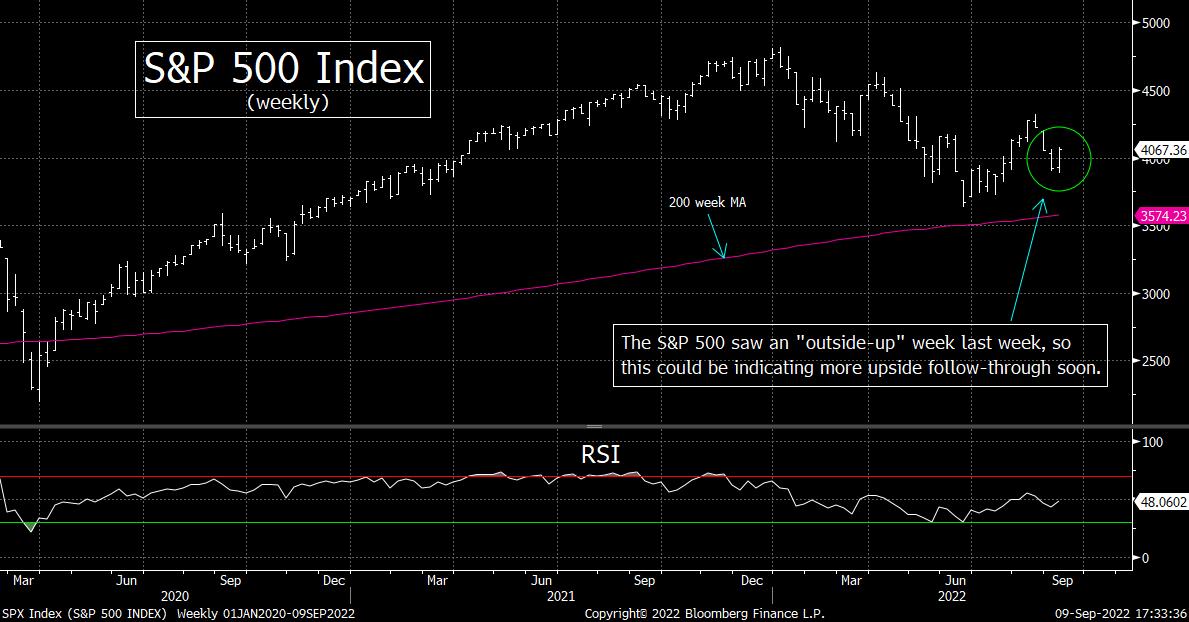

5) We did get some constructive action in the stock market late last week, so maybe we are wrong….and the stock market is going to resume the rally that began during the summer. The S&P 500 Index had an “outside-up” week last week, so this might be telling us that we’ll see a further rally over the coming weeks. Therefore, we don’t want to the entire time this weekend on the bearish side of the bull/bear ledger.

There are always two sides to every story, so we want to make sure to highlight some positive developments from last week on the technical side of things. Even though we believe that lasts week’s rally had more to do with the very-short-term oversold condition in the stock market, we did see a few things that could be telling us that the late-week rally will have some legs.

First of all, the volume during the three-day bounce was solid. No, it was not higher than what we saw during most of the late-summer decline, but it wasn’t any lower either. Also, the breadth of the rally was very strong on Friday. It was 9 to 1 positive on the S&P 500…and a whopping 33 to 1 positive for the NDX 100. Finally, all 11 of the S&P groups finished the day in positive territory. Thus, there’s little question that the internals of the late-week rally were quite good.

On top of this, the S&P 500 experienced an “outside-up” week. “Outside weeks” take place when the high for the week was higher than the previous week’s high…AND the low for the week was lower than the previous week’s lows…AND it closes higher than the previous week’s high. Outside weeks tend to show an exhaustion in the selling…and is usually followed by more upside follow-through. (Also, “outside-up” weeks tend to be much more compelling than “outside-up” days.)

We do need to point out, however, that the NDX did not see an outside week. When you combine this with fact that the SPX only achieved this outside week by a mere 4 points, it might be telling us that the upside follow-through (if any) will be short-lived…….However, on the flip side, if you combine the outside week…with the bullish internals from Friday…it’s still a positive development. Therefore, we felt it was important to point out this bullish potential as we hit halftime for the month of September.

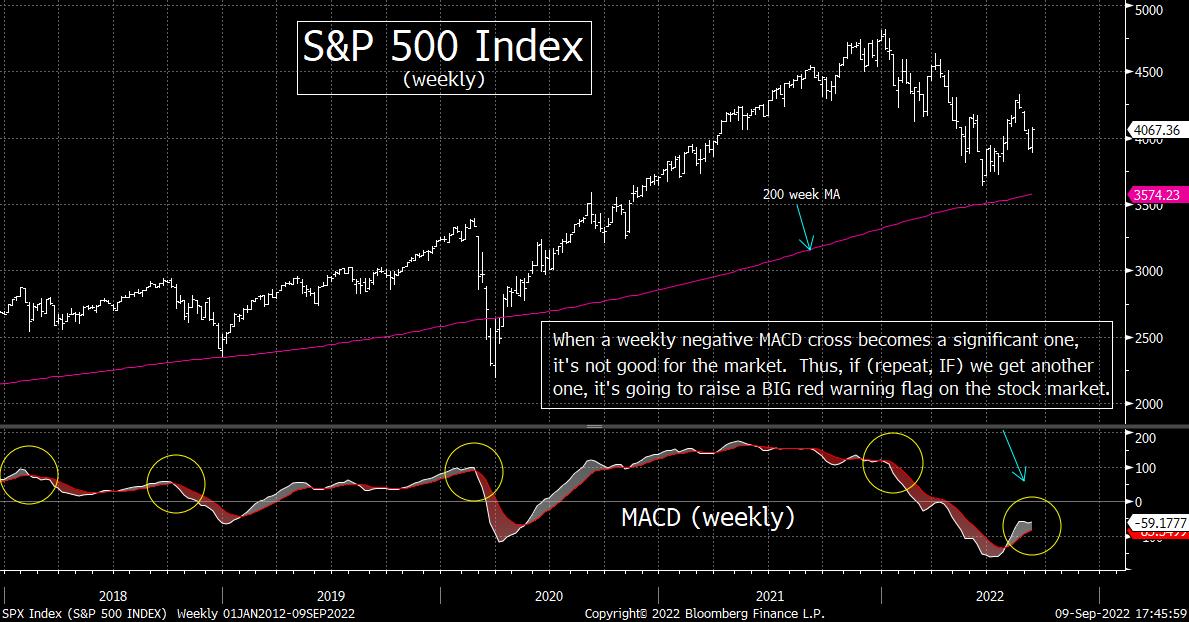

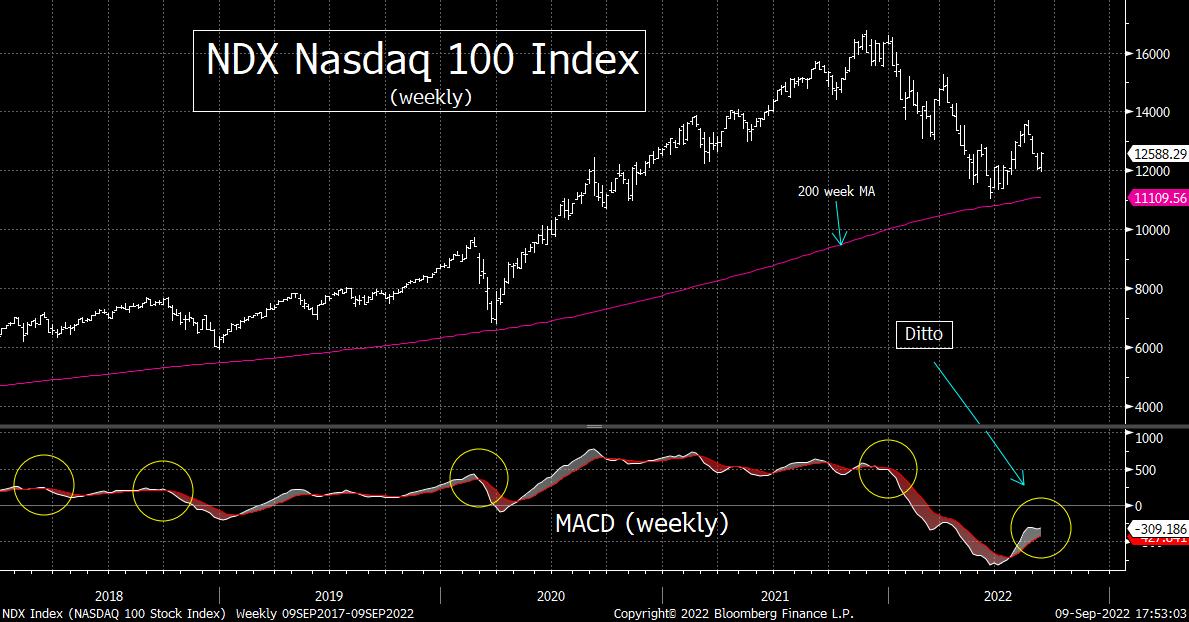

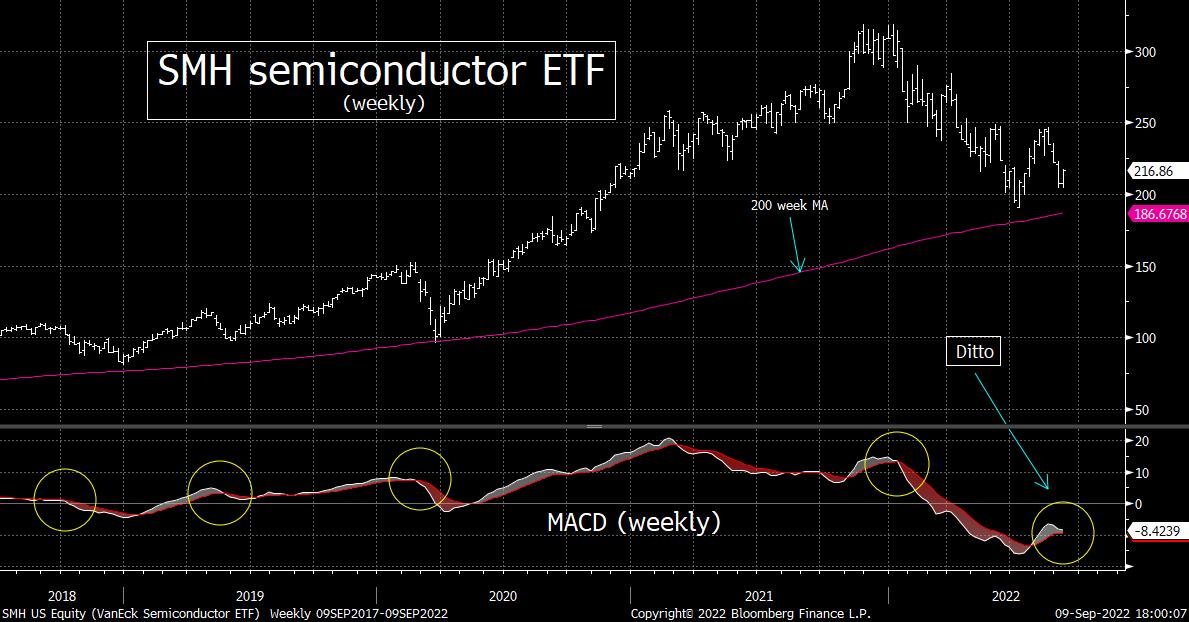

6) Even though we just discussed some more upside potential for the stock market, the S&P 500 Index, the NDX 100 Index, and the SMH semiconductor ETF (the most important leadership group in the market)…will all face some serious problems if (repeat, IF) they rollback over in a significant way at any point in the next several weeks.

As solid as the bounces were in the major averages were last week, they could easily just be seen as normal bounces from a very-short-term oversold condition…and thus the advances won’t last very long at all. The same is true for the SMH semiconductor index…which is the most important leadership group in the stock market.

As we highlighted in a couple of our recent “Morning Comments,” all three of these indices/ETFs had become oversold early last week. The NDX and SMH had fallen seven days in a row by last Tuesday…and the SPX had dropped 6 out of 7 days (with only a very small gain on that one day). On top of this, they had all declined between 9% and 16% in less than a month…and thus their RSI charts were reaching oversold levels as we moved into the middle of last week. Therefore, they were getting ripe for very-short-term bounces…and that’s what we’ve seen over the past few trading days.

They could see more upside follow-through early next week, but all of them have reached…or have almost reached…levels that could/should provide some key resistance before too long. This is particularly true for the S&P…where 4106 will give it a 50% retracement of its recent decline. As for the NDX, 12,643 is the level we’ll be watching…which will give it a Fibonacci 38.2% retracement of the Aug/Sept drop. Both are within whisper distance of those respective levels, so they might not see a lot more upside momentum going forward.

If (repeat, IF) these indices/ETFs do indeed roll-over soon, we’ll be watching the weekly MACD chart on all three of them. They have all curled over recently, but none of them has seen a negative cross. If they do, it will raise a big yellow flag for them on a technical basis.

However, we do need to point out that all of them have seen SOME negative crosses over the past four years that have been only very slight ones. Those were not followed by material declines…and some turned out to be outright head fakes. However, the ones that DID turn into meaningful negative crosses were followed by substantial drops each time. Therefore, if these weekly charts give us negative crosses that are more than just mild ones, it’s going to change any yellow flags into great big red one…very quickly…because it will confirm that the intermediate-term rally that we saw over the summer has come to an end…and that the momentum has moved back decidedly to the downside.

7) We have been very bullish on crude oil & the energy stocks for most of the past two years. However, we have stepped back from our bullish stance over the short-term on several occasions since October 2020. We’re going to do this once again right now…because we are seeing something in the chart on WTI crude oil which has us concerned.

Crude oil had a rough week last week. In fact, if it wasn’t for a strong 3% bounce on Friday, it would have been considered a horrible week. However, WTI did drop about 6% on Wednesday…and that gave the commodity a negative cross on its MACD chart. As you can see from the chart below, negative crosses have not been good for crude oil (or energy stocks) in the last year. On top of this, WTI also experienced a “death cross” last week…with its 50-DMA crossing below its 200-DMA. (Actually, the 200-DMA is still rising, so it’s technically not a “death cross.” You need to have both moving averages falling when the cross takes place. However, since the 200-DMA is only BARELY rising…and will be declining soon…it’s still a compelling development.)

Of course, this might be considered bullish for the broad stock market. The big rise in oil prices in the first half of the year got much of the blame for the bear market…and the significant decline in oil prices over the summer received a lot of credit for the bounce in stocks. Therefore, a further drop could be quite bullish for the stock market in the weeks and months ahead.

Then again, if the drop in crude oil becomes significant, it will likely signal that we’re going to have something that is much more than just a mild recession. A “soft landing”…at a time when oil output is significantly constrained…is not something that will cause crude oil to fall out of bed…especially if it has already fallen almost 40% and given back 2/3 of its 12-month rally! Therefore, a further meaningful decline from current levels would almost certainly signal that a much rougher recession than most people on Wall Street are looking for is on the horizon.

Put another way, history tells us that when we get a serious period of inflation, the situation plays out as follows: First comes the inflation…and THEN comes the recession. History also tells us that every recession since at least WWII has involved a decline in earnings. With the S&P 500 currently trading at 18x forward earnings, the stock market has not priced-in a recession. Therefore, if oil prices fall substantially further from current levels, it would be a strong indication that we’re headed for a rough recession…and thus the stock market will fall a lot further than it already has so far. (BTW, strong rally in crude oil over the past 50 years has been followed by a recession. Remember, oil fell in a significant in the middle of the bear markets of 2000-2003 and 2007-2009…and it didn’t keep the stock market from falling a lot further.)

Therefore, we think that investors need to be careful assuming that a further decline in crude oil will be bullish for the stock market. Of course, it could take time before the markets figure out that a meaningful drop below $80 is actually bearish for the stock market, not bullish. So, we could see more upside to stocks…for a little while…if crude oil does indeed decline a lot more.

However, we also have to admit that if the catalyst for a big decline in crude oil is the removal of sanctions on Russia, it WOULD be a very bullish development for the stock market. Thus, the technical picture the charts are painting right now might be bullish for the stock market. Of course, that would go against our bearish stance on the stock market right now, BUT we still believe it is important to highlight the situation to you this weekend. (The last thing we want to do is hide an important development…just because it doesn’t fit into our overall stance on the broad markets at any given time.)

Okay, we got side-tracked a little bit…by talking about what kind of impact lower oil prices might have on the stock market (much like we did with our comments about the currency market in point # 4). So, we want to get back to our original point…by saying that we are quite concerned about the price of crude oil right now on a technical basis. We have been very bullish for most of the past two years, but now is another one of those times where we want to be cautious on a short-term basis (much like we did in early June…and a couple of other times since we turned bullish on the sector back in October of 2020).

In other words, whether a further drop in crude oil will be bullish or bearish for the stock mark

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464