Can Financials Correct 30% From Their Highs?

When you talk about the U.S. Stock Market, a solid argument can be made that Financials are the most important sector. We always look to this space as a leader, as scary as that might sound these days. You can argue that Technology is technically more important because it has a slightly higher correlation with the S&P500 (0.97 vs 0.91) and also a little bit of a larger weighting in the Index (20% vs 16.6%), but for the purposes of this conversation, we’ll agree that Financials and Technology are without a doubt the most important sectors in the market.

Today we’re taking a look at Financials using a top/down approach. If we can get a good idea of where they’re headed, in all likelihood the broad markets will follow. The way I look at it, this sort of analysis can only help form a bigger picture thesis.

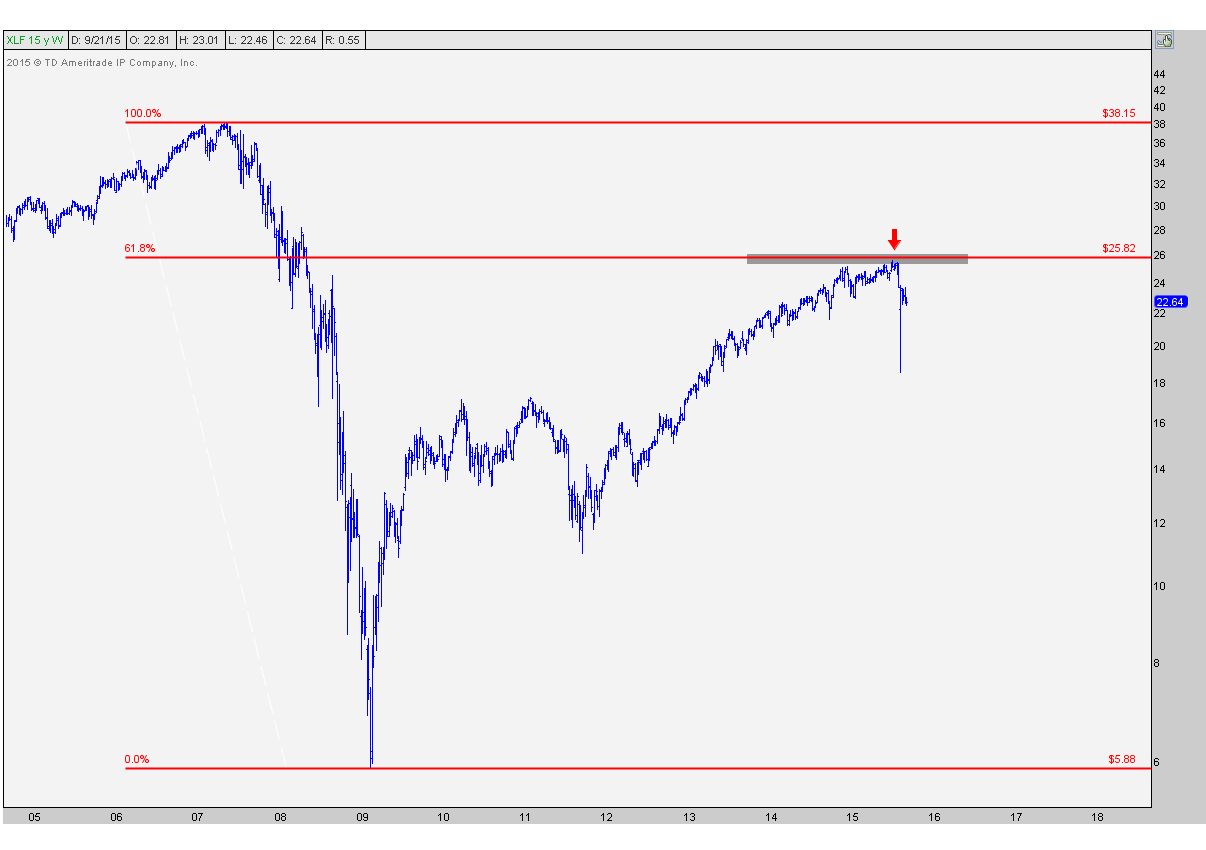

We’ll start with a longer-term look at the big boy $XLF which is made up of names like Wells Fargo (8%), Berkshire Hathaway (8%), JP Morgan (8%), Bank of America (5%), Citigroup (5%) etc etc. This is a weekly bar chart showing Financials rallying all the way up to exactly the 61.8% Fibonacci retracement of the entire 2007-2009 crash. Is this where we want to be buying? Or is this a level we want to be fading?

Looking shorter-term, here is a daily line chart showing prices trading below a downward sloping 200 day moving average. Assets in uptrends down trade below downward sloping 200 day moving averages. In addition we have a failed breakout in July that couldn’t hold for more than a couple of weeks. Long time readers know how much I love those. They suck in the last buyers that just through in the towel, whether they were on the sidelines or covering short positions, and then boom, the breakout fails. When you have these combined with a bearish momentum divergence, as is the case here, sharp declines tend to follow:

Notice how on the recent decline momentum hit oversold conditions after failing to hit overbought conditions on the breakout in July. Assets in uptrends don’t fail to get overbought. Assets in uptrends don’t get oversold. Also look at the uptrend line from the lows early last year that also broke. We now have overhead supply from all of that broken support from the past year as well as trendline resistance that broke last month and a downward sloping 200 day moving average over head.

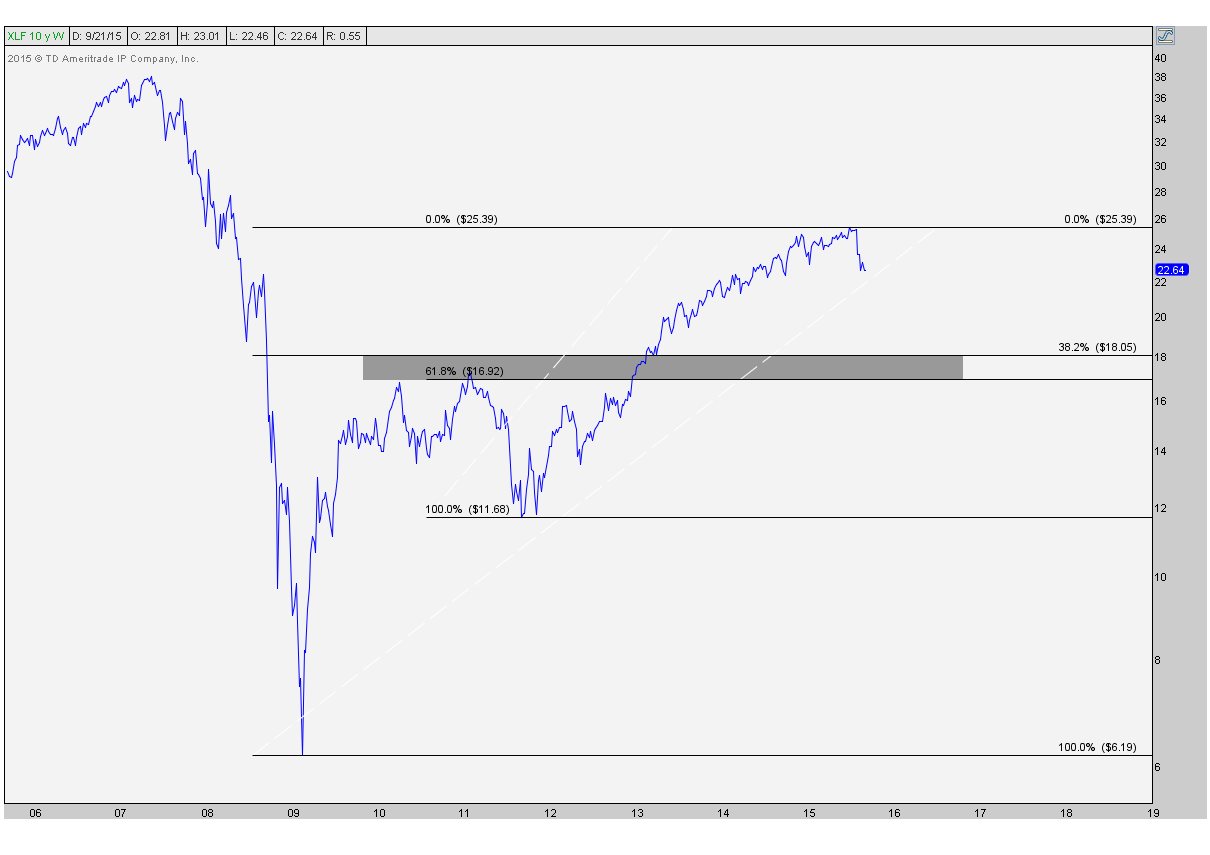

The weight of the evidence here suggests that 1) this is not in an uptrend and 2) we want to take any strength as an opportunity to sell into. How low can we go? I think we can see prices down near $17-18 and it wouldn’t be out of the ordinary. This area was former resistance in 2010-2011 and also represents a cluster of Fibonacci retracements which include the 38.2% retracement of the entire 2009-2015 rally as well as the 61.8% retracement of the 2011-2015 rally:

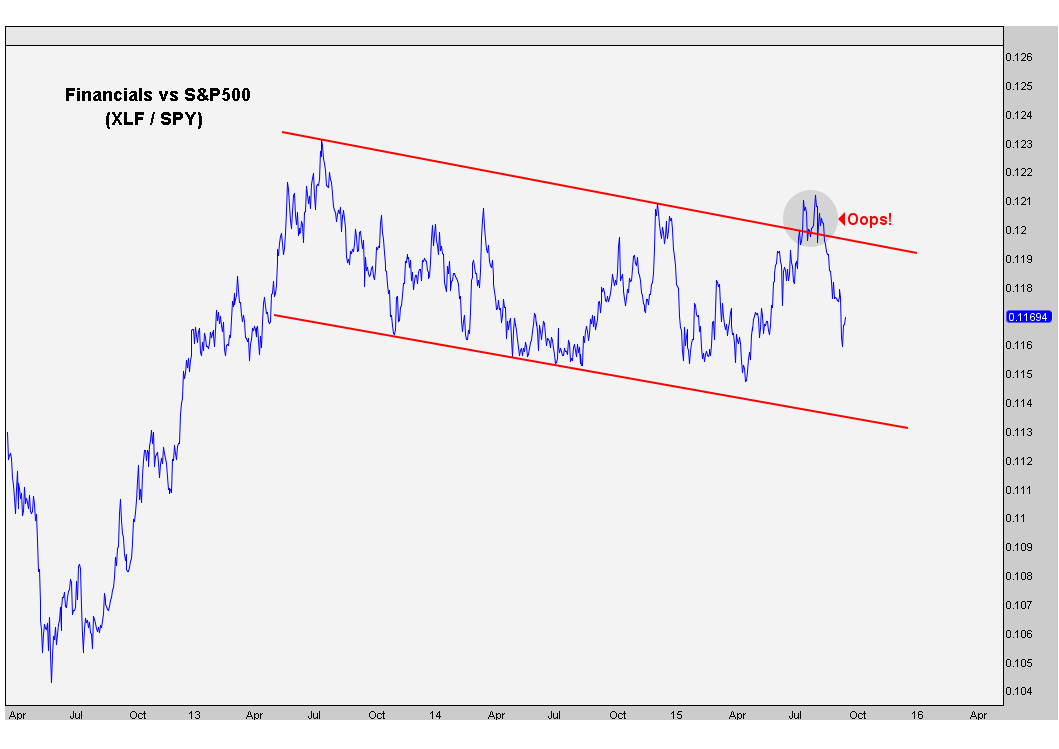

Now looking at the relative strength, in other words comparing Financials to the overall market, this is in a clear downtrend since midway through 2013. I often hear about Financials are outperforming, but the data suggests otherwise, particularly from an intermediate-term perspective. In fact, Financials attempted to breakout relative to the market this Summer and failed badly. You can see a false breakout and swift reversal above the upper of these two parallel trendlines defining the downtrend channel from the past couple of years. “From failed moves come fast moves in the opposite direction”, and this is precisely what we have here:

So what needs to happen for Financials not to have a correction of this magnitude? To me it’s time. There is a lot of damage that has been done based on the combination of a failed breakout and now prices below overhead supply and a downward sloping 200 day moving average. This isn’t good short-term and suggests fading strength is probably our best bet for now.

I always like to keep an open mind. I take the weight of the evidence and build a thesis. But along the way I constantly make counter-arguments against my conclusion and try and come up scenarios where the market will prove me wrong. For me, the counter argument here is pretty simple. If prices can consolidate sideways from some time, perhaps another month or so, without making new lows and then break out to the upside of that 2 month sideways range, it would allow the downward sloping 200 day moving average to flatten out and prices can continue to absorb that overhead supply. This could set things up for a larger base and ultimate breakout in the first quarter next year. This is certainly a possibility that I am open to. I just think it’s the lower probability outcome based on the weight of the evidence that we have today.

I think financials are heading lower. I want to be selling into any strength.

***

Click Here to receive weekly updates on each of these charts along with 30 more sectors and sub-sectors across the U.S. Stock Market including Technology, Energy, Healthcare and Materials.

Recent free content from J.C. Parets

-

Here’s Way I think Rates Are Heading Lower

— 11/12/15

Here’s Way I think Rates Are Heading Lower

— 11/12/15

-

Support & Resistance 101: Apple Edition

— 11/10/15

-

Video: Technical Analysis Webinar by JC Parets

— 10/01/15

Video: Technical Analysis Webinar by JC Parets

— 10/01/15

-

Find Your Edge: The Autumn 2015 AlphaShark Trading Symposium with a Presentation by J.C. Parets

— 9/25/15

-

Where Is The S&P 500 Heading Now?

— 9/09/15

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464