THE WEEKLY TOP 10

THE WEEKLY TOP 10

Table of Contents:

1) Fed tightening might not hurt the economy much, but it WILL hurt the stock market (further).

2) The Fed cares MUCH more about the credit markets than the stock market.

3) Trying to explain every short-term moves with fundamental reasoning is a big mistake.

4) Very, very little stress showing up in the financial system thus far. (That’s bearish for stocks!)

5) The dollar is on the brink of a change in trend.

5a) Can the EEM emerging markets ETF breakout to the upside soon?

6) 10-year yield testing key resistance…Banks getting quite overbought near-term.

7) HD is sending up a warning signal for the homebuilders.

8) Are inflation concerns causing consumers to pull in their horns?

9) Updates on the charts of the S&P 500, the Nasdaq Composite and the Russell 2000.

10) Summary of our current stance.

1) As he frequently does, Jamie Dimon made a VERY important comment last week…when he said that the economy can handle the Fed’s new tightening cycle. He very well could be correct. Although the Fed’s new tightening policy should weaken the economy somewhat, there is a decent chance that they can tighten without slowing down the economy in a substantial way. The problem is that Mr. Dimon’s comments are actually a good reason to be bearish on the stock market (even if you’re not bearish on the economy).

This past week, Jamie Dimon reiterated his positive stance on the U.S. economy…and took it one step further by saying that thinks the Fed’s new (more aggressive) tightening policy will not have a major negative impact on the economy. The fact that such a well-respected executive thinks the economy will remain strong despite the Fed’s big change in policy is certainly positive news, BUT it does not mean that the Fed’s policy change will not have a negative impact on the stock market! In fact, we have been arguing for a while now that it doesn’t matter what happens to the economy going forward, the Fed’s change from a MASSIVELY accommodative policy…to a restrictive one…will still cause the stock market to decline in a material way…even if the economy does not deteriorate in a significant way.

If you listen to what Mr. Dimon said (and what Fed Chairman Powell said in his confirmation hearings), they only discussed what kind of impact the change in monetary policy will have on the economy, NOT the markets. They just might be correct. Maybe (again, maybe), the economy can continue to grow at a nice clip. Sure, it could/should slowdown a little bit, but given that the economy is still coming out of a complete lockdown, it’s not out of the question that the economy can avoid shrinking. HOWEVER, we believe that stock market is so far ahead of the economy, that it will decline in a meaningful way…even if the economy doesn’t shrink…so that the market can move back down in-line with the underlying economy.

Okay, we DO have to acknowledge that to a certain degree, the stock market IS the economy. However, it sure seemed like Mr.’s Dimon and Powell were saying that the system is in such good shape that the economy will not be hurt as bad as it as in the past by a meaningful drop in the stock market.

In other words, if Mr. Dimon is correct…and the financial system and the economy are strong enough to handle some material adversity…THAT will actually be bearish for the stock market! Let us explain………For years, especially during the first several years following the Great Financial Crisis, the Fed could not let the stock market fall much at all…because the system was so fragile! This was even true in 2018…when the high yield market got hit so hard after the Fed raised rates once again in the middle of December that year. However, if this is no longer the case (as Mr. Dimon suggests), the Fed can drain some froth out of the market without much concern that it will create major problems for the economy…or turn the situation into another crisis. Therefore, Jamie Dimon’s bullish comments about the economy are actually bearish for the stock market…because it means that the “Fed put” is now much further “out of the money” than it used to be.

If there is no significant systemic risk on the horizon, it means the Fed will be willing to let the stock market fall further than they have in the past!....As we’ve said ad nauseam for weeks now, all you have to do is look at the extreme valuation levels to know that the Fed’s massive stimulus program had taken the stock market WELL ABOVE its underlying fundamentals. Forward P/E ratios, price-to-sales, market cap-to-GDP…you name it, the market is extremely expensive. Therefore, now that the massive stimulus that took the market to these extreme levels will be leaving the system, the stock market has nowhere to go but down…to get back in-line with the underlying economic growth rate…EVEN if the economy continues to grow.

The problem is that many investors believe that the vast majority of the rally since March 2020 has been related to fundamental growth. Sure, a lot of the rally has been fundamentally based, but certainly not all of it. In fact, over the pat 10-12 months, it has not been fundamentally based at all. By this time last year, the stock market had already surpassed its pre-pandemic highs by a wide margin, so all of the fundamental growth had already been priced-in a year ago! However, the Fed kept its emergency level of stimulus pumping…and THIS, not economic growth, took the stock market high for most of 2021.

Of course, most investors don’t like to admit to themselves that a market rally (that helps them make money) was artificially induced. (It was their “smarts” that made all that money…not anything artificial. It’s human nature to feel that way.)…..It’s kind of like what the NE Patriots are going through right now. They didn’t realize just how important Tom Brady was to their success. Sure, they know he was very important, but they thought that they had more to do with the success than they did. Therefore, they thought they were better players, coaches, business managers than they actually were. However, it was Tom Brady that made them all think they were a lot better than they actually were. THIS is what the Fed’s stimulus had done. It has made many investors think they were a lot smarter than they actually were.

(Don’t get us wrong, Bill Belichick IS a great coach…probably the GOAT. However, we also have to remember that when he won two Super Bowl rings as a defensive coordinator with the NY Giants, he had the greatest defensive player to ever play the game (Lawrence Taylor). When he won six Super Bowl rings with the Pats, he had the greatest offensive player to ever play the game (Tom Brady). Yes, he helped Taylor & Brady in an important way, but it’s the players play who play the games. If Tom Brady wasn’t so clutch at the end of six of his Super Bowls, the Pats might never have won any of them.)

It’s going to take a long time for investors to understand just how important the Fed’s massive stimulus programs helped the stock market in the months to come. Therefore, we’re going to see plenty of sharp moves in BOTH directions as we move through 2022. However, without the Fed (the LT and TB of the markets), it’s going to be all but impossible for the market to stay as far ahead of the fundamentals as it has been for most of the past 12 months. Thus, we believe that the stock market will see lower-los ….before a final bottom has been put-in.

2) Our comments in point #1 goes back to our belief that the Fed does not care as much about the stock market as much as they used to…or as much as many pundits think they do. Despite what most people think, this was also true in 2018…and thus we believe it is still true today. In fact, if anything, it’s even more true today.

It is our strong opinion that most people on Wall Street are mistaken when they think that the Fed will not let the stock market see a deep correction. They mistakenly believe that the Fed stopped their last tightening cycle because the stock market saw a correction. The facts say otherwise. As we have highlighted several times in recent weeks, the Fed KEPT ON tightening their policy in December of 2018…EVEN THOUGH the market was solidly in correction territory. At their mid-December meeting in 2018…when the S&P was down more than 13%, they STILL raised interest rates again! It was not until the high yield market started to crater a couple of weeks later (and credit spreads widened out in a dramatic way) that the Fed quickly “pivoted.” It was NOT the drop in the stock market that forced their hand, it was the move in the credit markets!

Before they began that last tightening cycle, one of the issues they sighted was the high valuation levels and the froth in the marketplace…as one (of several) reasons why they wanted to tighten. In other words, they WANTED the prices of some risk assets to decline…so that they could wring some froth out of the market and avoid another major bubble. Well, many Fed members have sighted the same issue leading up to this tightening cycle as well. Thus, we believe that one of the goals for the Fed this time around is to wring some froth out of several markets…including the stock market…once again.

Don’t get us wrong, their number one reason for their new tightening cycle is to rein-in inflation. However, given what they have said about valuation concerns, it sure looks like dampening asset price inflation is also one of their goals. However, even if we’re wrong…and it’s not one of their goals, the Fed KNOWS that the likely outcome of their tightening policy…because it ALWAYS has in the past! Therefore, even if it’s not a goal, it’s still something the Fed is comfortable with…and therefore investors should not be looking for the Fed to save the day on very little dip that takes place in the stock market over the coming months.

In fact, we believe the Fed will welcome the decline. If the stock market kept rallying the way it did from March 2020 through 2021, it would create the kind of bubble that…once it inevitably burst…it would create the kind of crisis that the Fed would find all but impossible to fix……….The Fed is doing the right thing (albeit late). They NEED to fight inflation…and they NEED to avoid another massive bubble. (Can you imagine what a 50% decline in the stock market would do in today’s marketplace…with the record levels of corporate debt that exists today…more than $11 trillion???)……..It’s very likely going to be painful, but it’s also going to be a lot less painful than it would have been if they had kept the pedal to the metal with their emergency levels stimulus program. (We cannot afford another bubble…which tend to result in 50% declines in the stock market.)

3) One of the problems many market prognosticators are having right now is that they’re trying to explain every short-term move in the market with fundamental factors. Sometimes the market merely becomes very overbought or oversold…and thus sees a very-short-term reversal…only to quickly return to its intermediate-term trend. We believe this is what took place early last week when the stock market bounced sharply (led by the tech stocks).

When the stock market bounced off its lows on Monday…and then continued to rally into the middle of the week…way too many pundits tried to explain the bounce using fundamental reasoning. We understand why people do this...it’s natural to think that the moves in the stock market are all fundamentally based. (That’s what we’re taught in school.)

However, the market frequently moves for many different reasons…especially on a short-term basis. It can become oversold or overbought. The positioning get become too one sided…and the same can happen with sentiment. All of these issues can and do have an impact on the stock market from time to time. (Sometimes by themselves…and sometimes working in concert with one another.)

Therefore, it is important to know when these issues have an impact. For instance, when the stock market bottomed on Monday, it was merely become somewhat washed out on a very-short-term basis. The Nasdaq had fallen over 8% on an intraday basis in less than 5 trading days…and the sellers had become exhausted. THAT is why the market bounced…NOT because it had fallen enough to make it cheap (or anything close to cheap).

Therefore, it was inevitable that it would roll back over rather quickly…and that’s exactly what it did later in the week. Nothing had changed in terms of the Fed’s new stance on their tighter monetary policy on Monday, so it was only a matter of time before the stock market rolled back over. (Sure, they tried to say that Powell said something a bit less hawkish, but that was only after the fact…when they needed to provide some reason the bounce. In reality, however, it was just a technical bounce.)

Of course, the stock market has been trading on non-fundamental issues since March 2020, so this is not just a short-term phenomenon. However, it will be vitally important going forward…with the Fed’s big change in policy…to understand what is really causing any bounce in the stock market. If a bounce is based on real “new news,” it could indeed signal and end to the drop in the stock market. However, if it is not…like it was not early last week…investors will need to be very careful. In fact, they’ll want to use those bounces as opportunities to raise some cash.

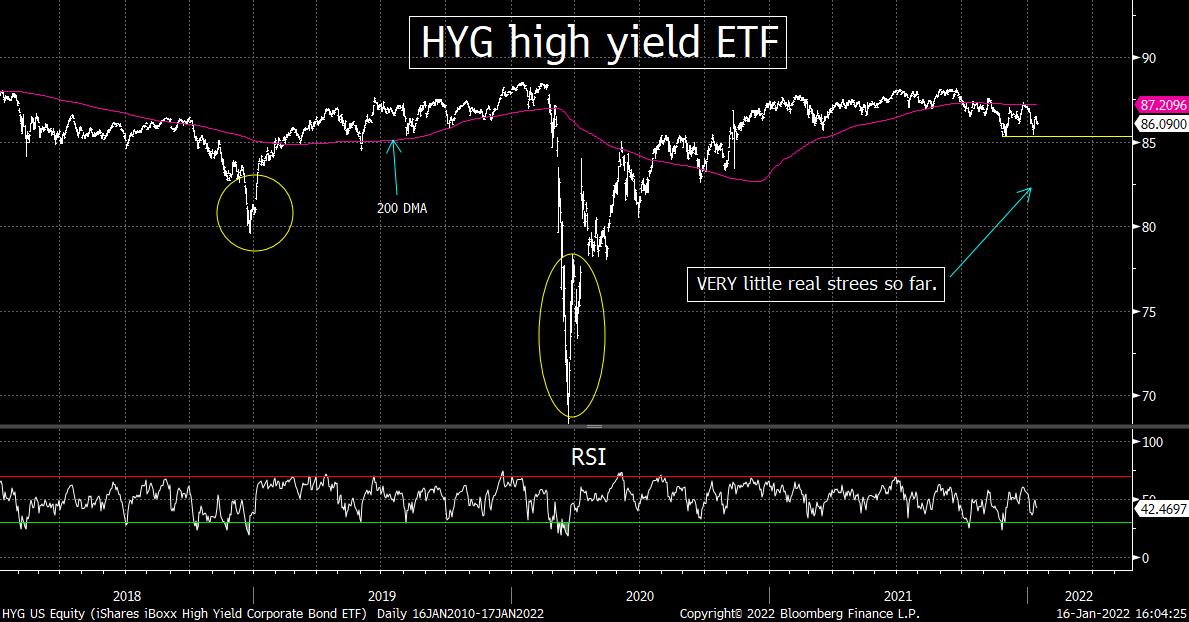

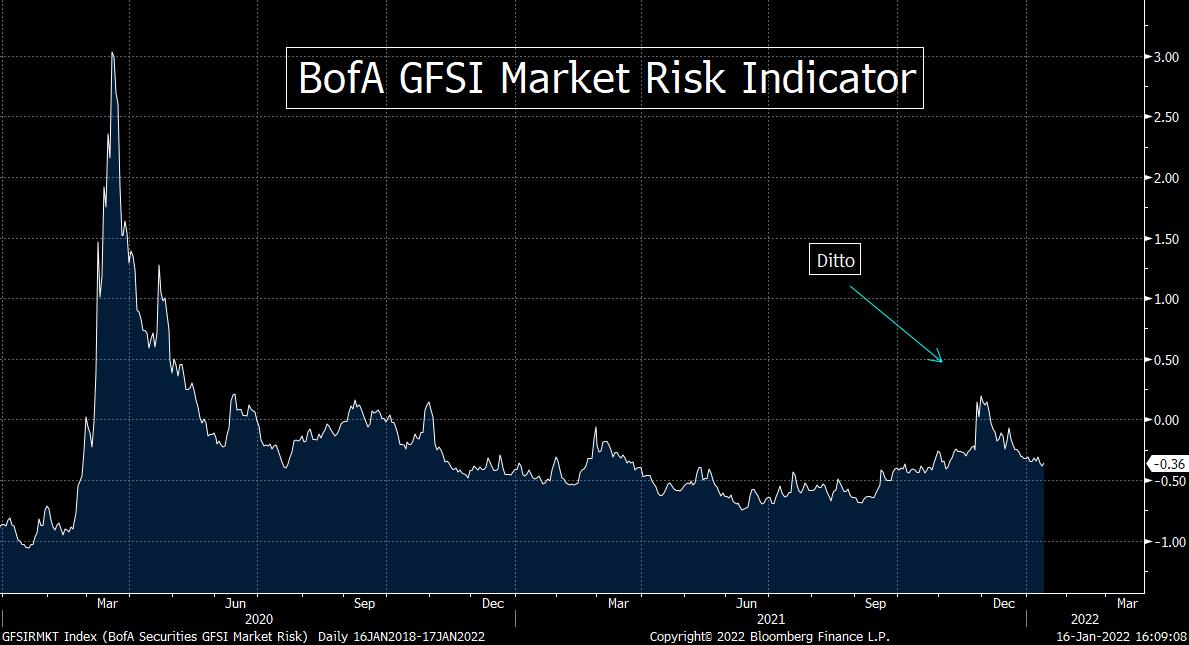

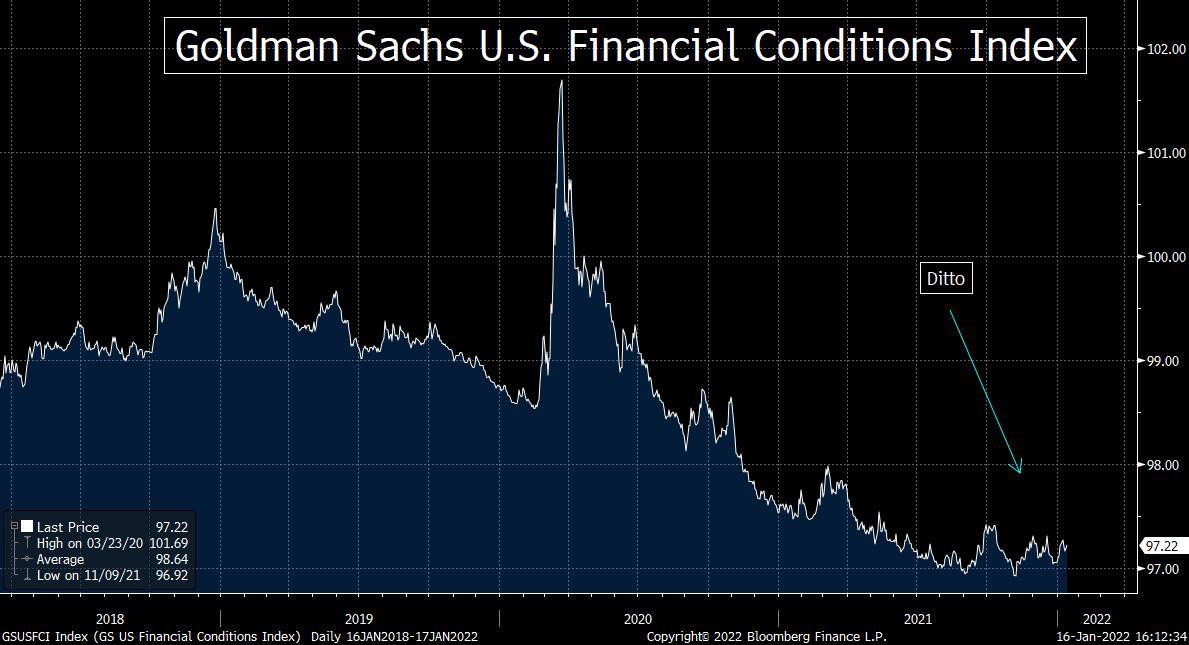

4) As you might expect from what we’ve said so far this weekend, we believe that it will be important to watch the credit markets for signs that the Fed might have to change its tone on its tightening policy. With this in mind, we’ll be watching the HYG high yield ETF…several credit spreads…and a couple of other stress indictors…to tell us when the Fed might “pivot” once again. Right now, most of these indicators are quite benign.

As we highlighted above (and in previous weeks), the Fed did not “pivot” in late-2018/early-2019 until some major cracks showed up in the credit markets. (They did not react to the stock market.) We saw the same kind of stress in those markets in March 2020. In fact, we also saw some stress in the early fall months of 2019…when the repo markets saw some considerable stress. That was followed by a QE program (that the Fed claimed was not a QE program)…which also led to a strong rally into the end of 2019 and early 2020.

However, we are not seeing much stress at all in these markets right now. Yes, the HYG has sold off, but it still stands well above its early December lows. Also, as we pointed out in point #2, we’re not seeing the price to insure junk bonds against default moving up much at all. In fact, as you can see from the charts below, we are not seeing ANYTHING approaching what we saw in March 2020 or the end of 2018 in other indicators of financial stress…like the Citi Marco Risk index or the BofA Global Financial Stress Indictor…or the Goldman Sachs U.S. Financial Conditions Index. None of these indicators are not raising any material concerns, so the Fed should be able to tighten in the kind of aggressive fashion they have been talking about recently.

We will be watching these indicators very closely in the weeks and months ahead. We’re sure they’ll show SOME increase in stress going forward, but unless they show some serious problems, the Fed is likely to continue to tighten their policy…EVEN if the stock market sees a correction (or worse) going forward.

5) It was a very rough week for the dollar last week. The dollar had actually been trading in a sideways range for almost two months going into last week (after a six-month rally), so it has already lost some steam. However, last week’s decline raised a big yellow flag for the greenback…and if it falls much further from here, it’s going to confirm a change in trend for our currency.

Early last week, we highlighted how almost nobody was talking about the weakness in the dollar in recent weeks. By the end of the day that day, that’s all anybody could talk about. No, we’re not saying that it was OUR comments to brought it to the forefront of everybody’s minds. It was a BIG drop that day…which took the DXY dollar index well below its 50-DMA…AND well below the sideways range it had been in since mid-November.

Theoretically, this should not have happened. The Fed’s new tightening cycle could/should create higher long-term interest rates…and that, in turn, should create a stronger dollar. However, as we pointed out, despite the change in policy from the Fed since November…and the more recent move to a more aggressive tightening cycle…the rally in the dollar has flattened out considerably between mid-November and early January. This is something we highlighted a couple of weeks ago, but after a very short-term bounce to start off the year, the DXY dollar index had fallen right back down to its lows of the previous two months.

In that comment early last week, we then highlighted that any break below the 95.50 level on the DXY would signal the beginning of a change in trend for the greenback…and a significant drop below 95 would confirm it. (95.50 had provided solid support for the dollar since the beginning of December…and 95.00 was where the trend-line from May 2021 came-in.)…..Well, not only did the DXY dollar index fall below its key 50-DMA support line…but it ALSO took it below its trend-line from last May (at the 95 level) on that very day!

That said, the dollar was able to bounce on Friday…and regain the 95 level by the close at the end of the week. In fact, the 100-DMA was the line that provided rock-solid support on both Thursday and Friday…and as just said, its bounce on Friday was a good one. Therefore, the 100-DMA is now the level we’ll be watching. However, since the DXY has broken well below its recent sideways range, it’s going to have to hold that 100-DMA or it’s going to raise a big red warning flag on the dollar on a technical basis.

Therefore, there is no question that the dollar is teetering right now…and if it falls further, it should have implications for some other markets.

5a) Needless to say, a further breakdown in the dollar should be bullish for commodities. However, that’s not the only asset class that could be impacted by a falling dollar. Emerging markets should also benefit if the dollar confirms a change in trend. In fact, the EEM emerging markets ETF is testing a key resistance level right now…and thus any upside follow-through would be quite bullish on a technical basis.

Not only will a change in trend for the dollar have an impact on commodities (as we highlighted yesterday morning), but it could/should also have an impact on the emerging markets. The EEM emerging markets ETF has rallied strongly over the past two days as the dollar has declined…and it is now breaking one key resistance level…and not far from another.

First of all, the 100 DMA provided very tough resistance in September, October and November…and it broke above that moving average yesterday. The break was not a major one, if it sees anymore upside follow-though, it’s going to be a bullish development for the EEM. We’d also point out that it is testing its trend-line going back to February of last year, so that’s another reason to say that any more upside follow-through will raise the odds that this asset class is going to run.

Having said all this, it will likely take a break above 52.0 to really confirm the breakout. A move above that level would take the EEM above its 200 DMA (which provided resistance in August and September of last year)….AND would give it a “higher-high.” So, that will be the more important level to watch.

Back to the U.S. stock market, this year has gotten off to a very volatile start…and we expect this to continue for the foreseeable future. In fact, volatility could pick back up very quickly…if the stock market reacts to the PPI number in the same way it did last month after that data hits the news-tape at 8:30 this morning.

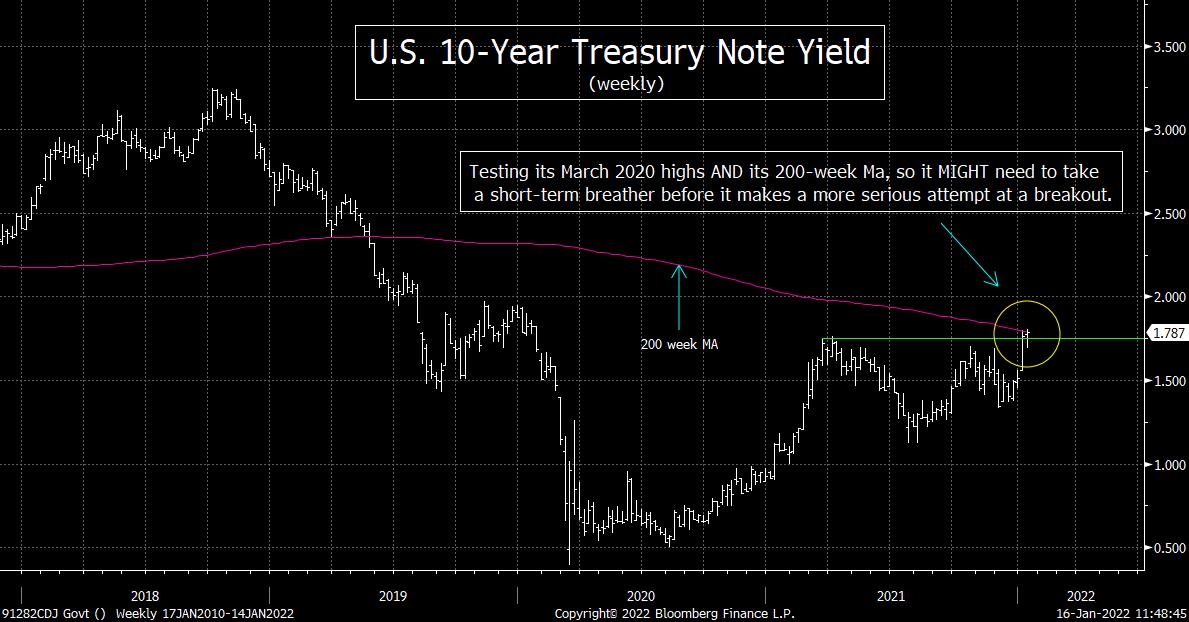

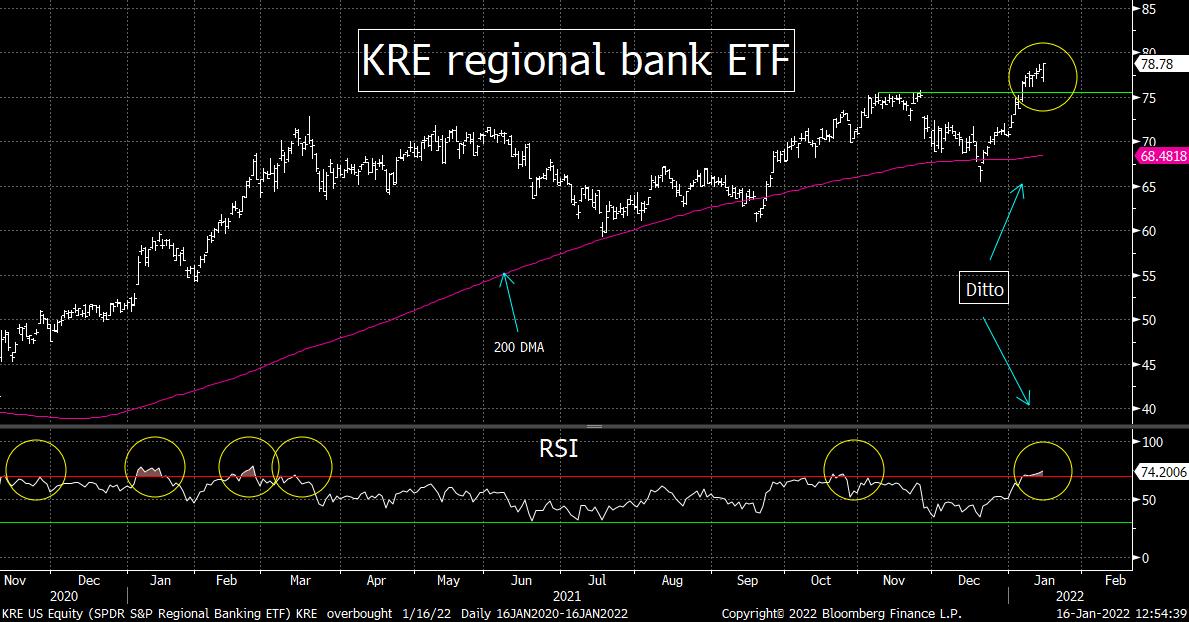

6) Next week could be a very important week for the bond market. Bond yields are getting pretty overbought, but more importantly, the 10yr yield is facing a VERY important resistance level. If this level provides strong resistance once again, It’s going to cause some near-term problems for the bank stocks (which are getting overbought). However, if the 10yr yield does indeed breakout, it’s going to cause problems for the broad stock market.

The Treasury market started the year with a very rough ride right from the get-go. The TLT Treasury bond ETF fell out of bed on the first day of trading for the year…and has remained under pressure ever since. Therefore, the yield on the 10yr note obviously jumped in a significant way as the year began…and it hovering near its recent highs.

The recent high for the 10yr yield is also the same level as we saw at the high from last March. Actually, the 10yr yield is slightly above those March 2021 highs, but since it only very slightly above that 1.74% level, it cannot be considered a “breakout” yet. It can only be seen as a “retest” of those 2021 highs so far.

We’re going to have to see more upside follow-through to say a breakout in rates has taken place. There is no guarantee that an upside breakout will indeed take place. The yield on the 10-year note is quite overbought…and when any asset tests a key resistance level at ta time that it is overbought, it frequently has to take a “breather”…to work-off that overbought condition…before it gives us a confirmed breakout.

However, we’d also mention that not only is the 10yr yield testing its March 2020 highs, but it’s also testing its 200-week moving average. Therefore, since this 1.75-1.80 range is an important resistance on TWO different key readings, it might indeed have to take a breather…and see a pullback…before it takes a more serious run at breaking out to an important “higher-high.”

On the one hand, a pullback in long-term rates should be bullish for the tech stocks and the broad stock market. However, we also have to acknowledge that a pullback in rates COULD take place due to a “flight to safety” move in the Treasury market…in reaction to big decline in the stock market. Thus, it is not a lock that a drop in rates will be a bullish development. However, THAT kind of move will almost certainly be negative for the bank stocks on a short-term basis. In fact, a decline in the 10yr yield (especially if it coincides with a further flattening of the yield curve) should be negative for the bank stocks on a short-term basis NO MATTER WHAT the reason for the decline might be.

The reason we highlight this potential is because the KBE bank ETF has become overbought near-term. Its RSI chart has moved up to the 73 level…which is very close to the same level that has been followed by short-term pullbacks over the last five years. This does not mean that is will impossible for the banks to rally a little bit more before they take a breather, but we just think that investors should be careful about chasing this group over the next week or two.

Don’t get us wrong, we still like the bank stocks on an intermediate/long-term basis, so we’re not saying investors should take profits on the group. We’re merely saying that they should think about being a bit less aggressive over the next week or two. Yes, they can still nibble on the group, but it’s probably going to be a better idea to hold off in being aggressive on the banks until that see a pullback over the coming 1-3 weeks.

The KBE and the KRE regional bank ETFs both opened lower on Friday (after the negative earnings reports out of JPM and Citi), but they both bounced strongly and finished higher by the close. The main reason why they bounced so strongly (even though JPM & Citi remained in negative territory all day) was because of the big jump in Treasury yields. If those yields come back down next week…for whatever reason…those ETFs should indeed see some weakness…..Not only will they feel pressure from lower yields, but they always seem to act poorly when the group announces their earnings. So this is another reason to be a bit careful about banks over the next week or two (or three).

Of course, if bond yields DO breakout next week in the face of their overbought condition, it will theoretically be good for the banks stocks. However, since an important upside breakout in long-term interest rates is likely to be quite negative for the broad stock market, these bank stocks could still face some short-term headwinds. (If the indexes get hit hard, ALL of the stocks in the indexes will go down with them. The banks could still outperform as they drop, but they’ll still be falling…so we think that being a little less aggressive on the group near-term will be a good idea.

As we re-read what we’ve said in this bullet point, it seems like it could be a bit confusing. What we’re trying to say is that the banks are overbought and thus vulnerable to a short-term pullback. In fact, the group could decline even if yields rise…because a breakout in yields will likely hurt the broad market. At some point, a significant drop in a key index like the S&P 500 will hurt all stocks. Therefore, we think investors should hold off on being aggressive on the bank stocks near-term…and look to get more aggressive on dips.

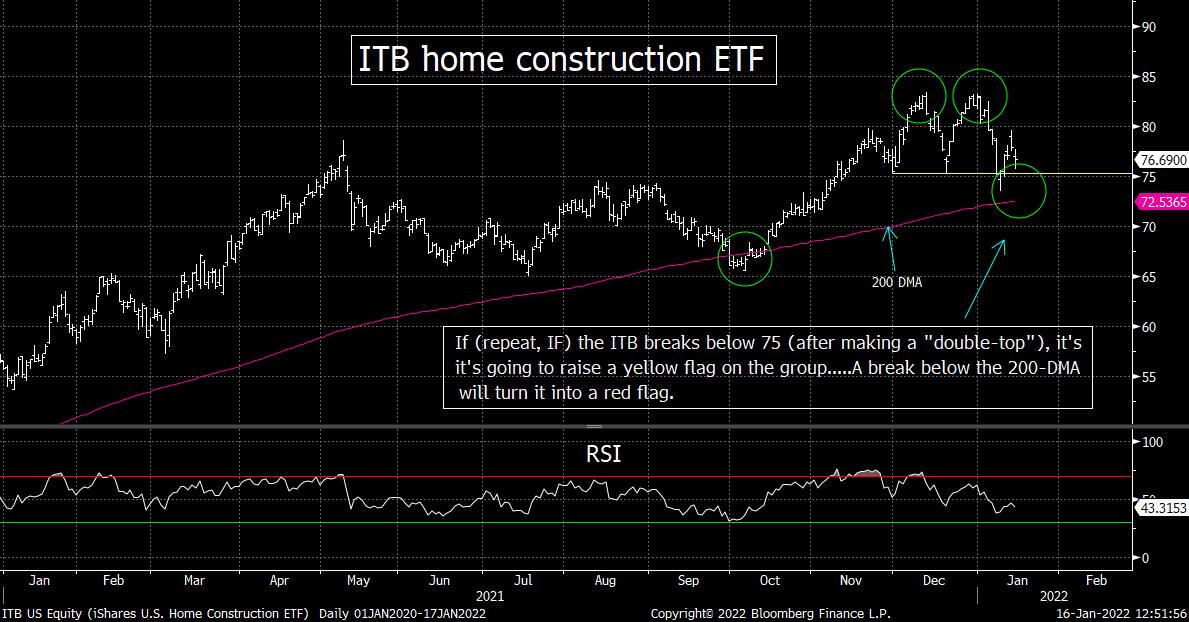

7) We are starting to get a little worried about the homebuilders…even though KB Homes (KBH) reported excellent numbers last week. Higher interest rates seem to have weighed on the group since the beginning of the year, but whatever the reason might be, there’s no question that the ITB home construction ETF is not far from a key support level. If it breaks below that level in any meaningful way, it will raise a yellow warning flag on this key group for the stock market…at least over the near-term.

We remain quite bullish on the housing sector on a longer term basis. Hard assets, including one’s home, were a great inflation hedge for people back in the 1970s. However, this does not mean that the sector will rally in a straight line over the coming months and years. We are starting to see some cracks in the ITB home construction ETF…and so if we see any further weakness in the group, it’s going to raise some concerns in our minds about the short and intermediate-term potential for the housing stocks.

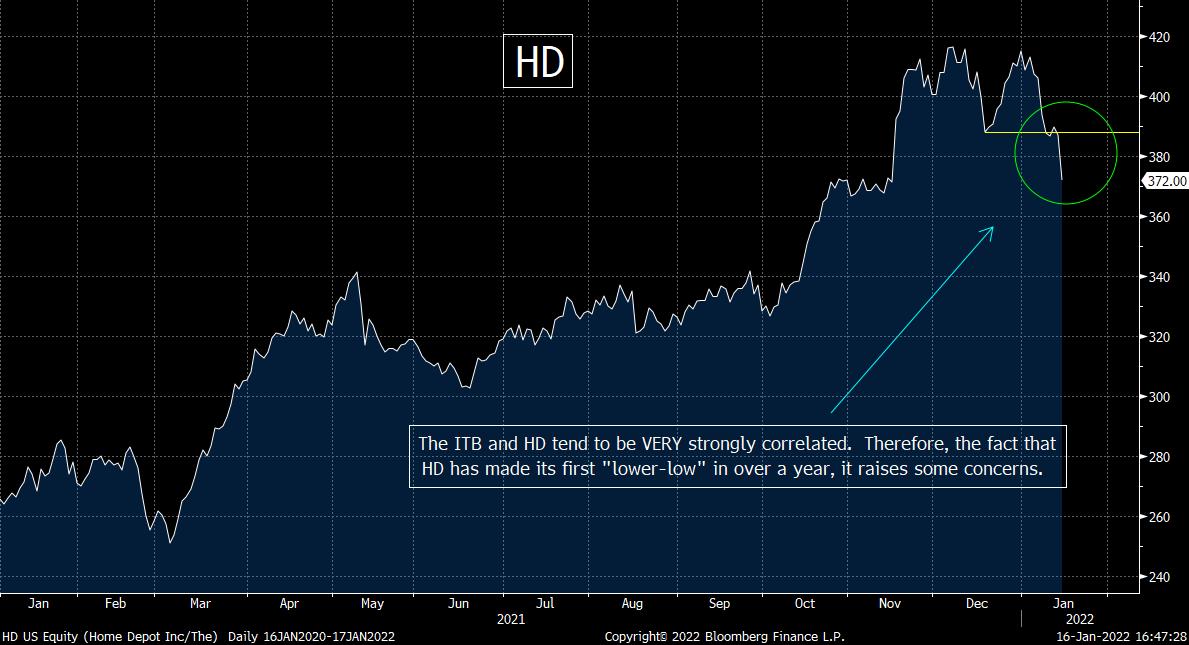

Last week, KBH reported excellent earnings…and the stock jumped 16% that day…and finished the week with a 23% gain! However, despite the move in that stock, the ITB was only able to rise 1.9%. In fact, it closed 3.6% below its highs from last week, so the news from KBH was not enough to give it a sustained rally last week……On top of this, we noticed that lumber is getting overbought…and HD (which had a stellar performance in 2021) has fallen more than 10% already this year…and made a key “lower-low.”

What we’re going to be watching is the 75 level on the ITB. That was the low for the ETF on November 30th, December 20th and at the beginning of last week. Therefore, if it breaks below the 75 level, it will give it a key “lower-low” and thus it would be quite negative for the housing stocks. This is particularly true given that the ITB made a “double-top” up near the 84 level in December. In other words, if it follows thie “double-top” with a key “lower-low,” it will definitely raise a big yellow flag on the housing sector.

The other level we’ll be watching in the 200-DMA on the ITB. That moving average provided excellent support for the group back in early October. Therefore, if it breaks below THAT line in the coming weeks, it will change the yellow flag into a red one.

Having said all this, we CANNOT get ahead of ourselves. The ITB has not yet fallen below the 75 level…and its still more than 5% above its 200-DMA. In other words, if the group can get some more good news out of some other companies (like it did last week from KBH), maybe the group can bounce strongly and take out that “double-top” high from December. However, with HD under such severe weakness…and with lumber getting overbought…a case can be made that the home construction sector will see a bit of a rough patch before it returns to its long-term upward trend.

8) Recently, we highlighted how…despite all the talk about how strong the U.S. consumer is today…the XRT retail ETF has badly underperformed the stock market since mid-November. Well, looking at last week’s retail sales report…and the continued weakness in the XRT (AND the XLY consumer discretionary ETF)…we have more evidence that the consumer is losing its strength as we move into 2022.

Despite all of the talk (for many months now) about how the U.S. consumer remains very strong, the consumer related stocks have not acted very well at all. On top of this, we received negative news last week about retail sales and consumer confidence. None of this bodes well at a time when inflation is rising to a level not seen in almost 40 years.

On Friday, we got the retail sales data for December…and they stunk. The headline number was -0.9% vs. the consensus expectation of -0.1%...and the ex-auto number was -2.3% vs. an expectation of +0.1%!......Later in the day, we heard the University of Michigan Consumer Confidence number. It was 68.8 vs an estimate of 70.0…and the data for “

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464