THE WEEKLY TOP 10

THE WEEKLY TOP 10

Table of Contents:

1) Lower asset prices do not mean the Fed has made a “policy mistake.”

1a) The last time the Fed tightened; they didn’t worry about the stock market.

2) Massive stimulus = more risk, more leverage. Less stimulus = the exact opposite.

3) The HYG high yield ETF is close to a key resistance level. Upside breakout coming?

4) We see higher long-term rates next year. Here are the key levels to watch.

4a) We’re cautious on the bank stocks on a near-term basis.

5) The dollar is showing some signs that its multi-month rally could end soon.

6) The energy sector looks good on both a fundamental and technical basis.

7) The chip stocks just might see a surprising decline in the first half of 2022.

8) Will institutions come back to cryptos and help them rally in early 2022?

8a) Gold is not far from two different important resistance levels.

9) Why are the defensive consumer staples group acting so well recently?

10) Are the retail stocks telling us something surprising about the consumer next year?

11) Bill Gates and his friends are still clueless.

12) Summary of our stance for 2022.

1) One of the biggest fears that many investors have is that the Fed might be making a “policy mistake” by tightening right now. The problem with this thinking starts with the assumption that if the stock market were to see a deep correction, it would confirm that the Fed had indeed made a “mistake.”…..We hate to say it, but sometime the absolute correct thing to do for the Fed is to engage in actions that will cause the economy to slow somewhat…and thus precipitate a decline in asset prices. In other words, those investors who think they Fed always wants to keep risk asset prices rising (or think that it’s the Fed’s job to do so) are the ones who are making a big “mistake.”

The term “policy mistake” is used much too freely in the marketplace today. Yes, the Fed has certainly made “policy mistakes” in the past, but this has to do with the impact their policies have had on the economy, NOT the stock market. Just because a shift in policy ends up being negative for the stock market (or other asset prices), it does not make it a “policy mistake.” (In fact, if a change in policy actually causes a slow-down in the ECONOMY (and not just a fall in asset prices), it does not necessarily mean the move was a “mistake” either…if it helps the economy (and thus the markets) on a longer-term basis.)

Let’s face it, when Volker’s Fed tightened policy dramatically several decades ago, it badly hurt the stock market…and created a sluggish period for the economy. However, it was NOT a policy mistake…for the simple reason that it was EXACTLY the right thing to do for the long-term health of our economy. (Therefore, even though it was bearish for stocks over the short/intermediate-term, it was bullish for the stock market on a very long-term basis.)

We are facing a similar situation today. We have a situation where inflation has been rising significantly for a long time now…AND asset price inflation is reaching a boiling point. (Some assets are already in bubble territory…and it won’t take much more upside moment in others to reach bubble levels.) Therefore, the Fed is doing the right thing by ending their QE program and raising rates (in the future). If they don’t move now, it will raise the risks significantly that inflation will get out of control and will kill consumer demand…in our consumer-led economy…….They will also risk creating another major asset bubble…which will have a disastrous effect on the economy once the inevitable bursting of that bubble takes place.

In other words, it would be a much bigger “policy mistake” that could if the Fed DID NOT tighten monetary policy. Yes, we can debate whether the Fed should have tightened earlier or not…and whether the impact would have been lighter if they had indeed acted earlier. However, we believe it is much more important to focus on the situation we ARE facing today…not the one we SHOULD be facing.

This is a long-winded way of saying that what the Fed is doing will very, very likely slow economic growth…at least somewhat. It is also VERY, VERY likely hurt the (extremely expensive) stock market. However, this will NOT make it a policy mistake.

The Fed’s job is not the create endless economic growth and an ever-rallying stock market. Instead, (on top of propping up their owners when needed), the Fed’s job is to help smooth-out the imbalances that INEVITABLY crop up in the economy in a capitalistic society……Economic weakness…stock market declines…company failures…etc…are an important part of capitalism. Thus, it’s not the Fed’s job to help everybody make money in the stock market all of the time!!! In fact, sometimes their job is to do the exact opposite…and we believe that those investors who don’t understand this are very likely to get burned in the coming year.

1a) The last time the Fed tightened, one of their main goals was to take some of the froth out of the markets. They did not care that the stock market went down. In fact, based on what Powell and other FOMC members said during 2018, they wanted it to go down. It was not until some significant cracks appeared in the credit markets that the “Powell pivot” took place…and the Fed reversed their tightening policy.

Way too many people believe that the Fed reversed their tightening policy of 2018 (with the “Powell pivot”) back in very late-2018/early-2019…because the stock market was falling in a significant way. This thinking is dead wrong in our opinion…and the facts bear us out. Just look at what took place in Q4 of 2018. At the December Fed meeting of that year (in mid-December), the stock market was already getting hit hard. In fact, it was already in correction territory…and yet Chairman Powell STILL raised interest rates again at their December 15th meeting. In other words, the stock market’s decline did not concern them at all!!!!

It was not until the high yield market fell out of bed…and credit spreads widened out significantly (in the last two weeks of December) that the Chairman changed his tone…and the Fed changed their policy soon thereafter.

Given this past example…and given what the Fed is saying right now…we think investors should not assume that the Fed has the backs of stock investors to the degree they have through much of the past 15 years. Instead, we think the situation is much like it was in 2018….with many members of the FOMC have said in recent months that they are concerned about the high level of asset valuations (and these concerns have shown-up in the “minutes” of several Fed meetings). Thus, we believe that the “Powell put” is much further out-of-the-money than it has been over the past 21 months…and for most of the past 12 months. Instead, we believe the safety net sits at a much lower level than most people realize…just like it did in 2018.

We’d also note that several members of the Fed…including NY Fed President Williams…have talked a lot about how the financial system is in very good shape. This was not something they could say in the year immediately following the financial crisis…and that’s why they had to follow QE1 with QE’s 2 and 3 in the first half of the last decade. To us, this signals that the Fed believes that the system can withstand a decline in asset prices to a much better degree than it could 8-10 years ago. Thus, this is another signal that the Fed is not overly concerned about a decline in the stock market.

Having said all this, we do understand that the Fed will be playing a tough balancing act. If the stock market falls IN A DRAMATIC FASHION (like it did in March of 2020), the drop WILL have a compelling impact on the economy…and on the credit markets. Therefore, it’s going to be difficult for them to reach the right balance…where they can slow the growth of inflation and wring a lot of the froth out of the markets…without creating another crisis. However, those who think the Fed’s goal is to make sure the economy never slows down again…and/or that the stock market will rally forever…are out of their minds. (That kind of goal is impossible in a capitalistic society…and the Fed knows it.)

In other words, the “Fed put” has not gone away, but we do believe that it is much more out-of-the-money that it has been for most of the past 10-12 years…(and just like it was the last time they tightened policy).

2) None of what we have said so far means that we’re definitely headed for a recession or a bear market. The Fed’s new policy might not hurt the economy much at all. However, that does not mean that it will not create an outsized decline in risk assets…including stock prices. Stocks have moved so far ahead of their underlying fundamentals that they could decline in a meaningful way…even if the fundamentals do not deteriorate much at all.

We have shown many times in these pages how the stock market has moved well beyond their fundamentals. Therefore, now that the Fed’s massive stimulus program is the process of reversing, stock prices will have to fall to a level that is more commensurate with their true fundamentals, in our opinion.

We realize that it’s human nature to think that as long as the economy continues to improve and that earnings continue to grow, the stock market has no place to go but higher. The reason it’s human nature is because when the economy improves after a down-turn that is usually what happens. The problem today is that there is a big difference between what usually transpires and what is taking place today. The stock market is usually flat on its back (or at least just beginning to rise from an important low). That is not what took place this time around. Long before the economy moved back towards its pre-pandemic level, the stock market has already bounced in a significant way.

That’s right…back in early August of 2020…when thousands of summer vacations had been cancelled…and restaurants were running at 25% capacity…and there were no vaccines available…the stock market had already taken back EVERYTHING it had lost from the pandemic!

Sure, we understand that the stock market is a leading indicator for the economy, so it should have started to bounce back before the economy had turned around. However, when was the last time the stock market recovered 100% of an economically induced decline so quickly? It would have been one thing if a vaccine had already been developed, but since it hadn’t been, the kind of massive rally that took place over the previous 4-5 months was artificially induced.

We think it’s safe to say that everybody KNEW that market was trading at an artificial level in the summer of 2020. None of us minded, because we believed that the economy would catch-up rather quickly. The problem is that once the economy had begun to play catch-up in a material way (in the first half of 2021), the artificial stimulus just kept on coming. In other words, if the stock market has stopped rallying at a level that was at/near its pre-pandemic levels…and had been left to trade on its own (instead of leaving emergency levels of stimulus in place)…the fundamentals would have been able to catch up to the stock market. However, since that stimulus never subsided, the stock market kept on rallying. This means the market has STAYED well above its fundamental levels…and the economy has not been able to play catch-up to the stock market.

Again, it is human nature to think that an improving fundamental backdrop will keep the rally going…but that’s only because it’s also human nature to forget that the success investors have experienced over the last 21 months was due in large part to artificial reasons. People like to think they made all that money because they were smart…not because the Fed kept providing the market with steroids. (NO, we are NOT saying that ALL of the rally since March 2020 has been induced by stimulus. A LOT of the rally was based on the rebound in the fundamentals. We’re just saying that the Fed’s continued emergency level of stimulus played important role in the OUTSIZED rally in the market.)

Since it is human nature to ignore how much the stimulus helped push stock prices higher, it is human nature to think that further fundamental improvement will create a further rally in stock prices. However, since the market is so far ahead of its fundamentals, the stock market could actually decline EVEN if the fundamentals do not deteriorate. (In fact, the market could theoretically fall even if the fundamentals continued to improve.)

Of course, our call is that the Fed’s tightening policy will indeed cause a slowdown in growth. However, even if it’s not a significant slowdown, the stock market could/should still see a deep correction or even a bear market.

All one has to do is look at the valuation levels. If the stock market had caught up to the fundamentals, the S&P would not be trading at almost 22x 2022 earnings estimates…more than 3x sales…and at a record level of market cap-to-GDP…..There is no question that valuation levels are lousy time tools, but they become much better ones when the Fed changes their policy to one of tightening (ESPECIALLY when they are moving from an ultra-stimulative policy…and not just a neutral one like they usually do.)

3) After a rough November, the high yield market bounced back VERY strongly in December. The HYG high yield ETF did not regain its all-time high from September, but its bounce was still a very strong one. On the technical side of things, it has formed a pattern which, if broken to the upside, will be very bullish. Given how highly correlated the high yield market and the stock market have been historically, an upside breakout would be quite bullish…so (as usual), there are still plenty of issues that stand on the bullish side of the bull/bear ledger right now.

One of the biggest concerns for the stock market this fall was the poor performance of the high yield market. The HYG high yield ETF fell quite sharply in November…and this led to a decline to its lowest level of the year. One of the things that made this decline particularly concerning in November was the fact that high yield spreads were incredibly tight (and yields were incredibly low)…which raised concerns about too much froth in that risky market. (This is something that is still a concern for many investors.)

However, the strong bounce in the HYG has given the marketplace a lot of relief in the past month. We’d also note that the HYG has formed an “inverse head & shoulders” pattern since late September…with its 200-DMA acting as the “neck-line” of this pattern. Therefore, if (repeat, IF) the HYG can break meaningfully above that line (and hold above that line), it should be quite bullish for this asset class…..Given the high correlation with the stock market, it should be bullish for stocks as well.

Of course, one of the most bearish developments can be a failed inverse H&S pattern (just like a failed H&S pattern can be incredibly bullish)….so we will need to guard against another quick reversal in the high yield market. However, there is no question that the action in this asset class over the last month has been quite positive.

4) We believe that volatility will be high in the bond market next year as well. High inflation and the end of QE should push long-term interest rates higher. However, we should also see some sharp declines in rates along the way…as investors play the “flight to safety” trade from time to time when the stock market declines in a significant way. We have some key levels to watch to see if the 10yr yield is indeed going to rise next year.

There is no question that long-term interest rates have risen significantly over the past 18 months (from 0.5% to 1.5%). That said, those yields are also sitting at a level that is equal to where they stood in March of this year. No, we’re not trying to say that long-term yields have not moved much over the past 9-10 months. They did jump towards 1.8% during the spring months…and then rolled-over and fell below 1.2% by the end of the summer. We’re just saying that even though the 10yr yield is back to the 1.5% level it stood early in the spring, there HAS been volatility in the Treasury market this year.

Even though long-term interest rates are still quite low on an historical basis, they’re much higher than their 2020 lows of 0.5%. More importantly, we think they’re headed higher. By March, their massive QE program will go from buying $120bn of bonds per month…to zero. Therefore, the supply/demand equation is going to shift in a serious manner. On top of this, inflation remains elevated. A lot of people think that once the supply chain issues subside, inflation will return to pre-pandemic levels (or at least something resembling those levels). We disagree.

Wage inflation is not going away. We have about 7 million people who are unemployed and almost 11 jobs that are available. Why are they not taking these jobs…even though some of the benefits have disappeared? Well, a lot people can make as much money driving for Uber or delivering food for Uber and others, that it is not worth it for them to take many of the jobs that are indeed open. (We hear a lot of complaints about finding childcare. Do you know how little many childcare providers get paid??? It’s easier to those former childcare providers work with Uber, Lift, Grubhub, Doordash, etc.)……If you listened to the earnings conference calls with companies like Amazon and Starbucks, you know that wage pressures are having an important impact on these companies.

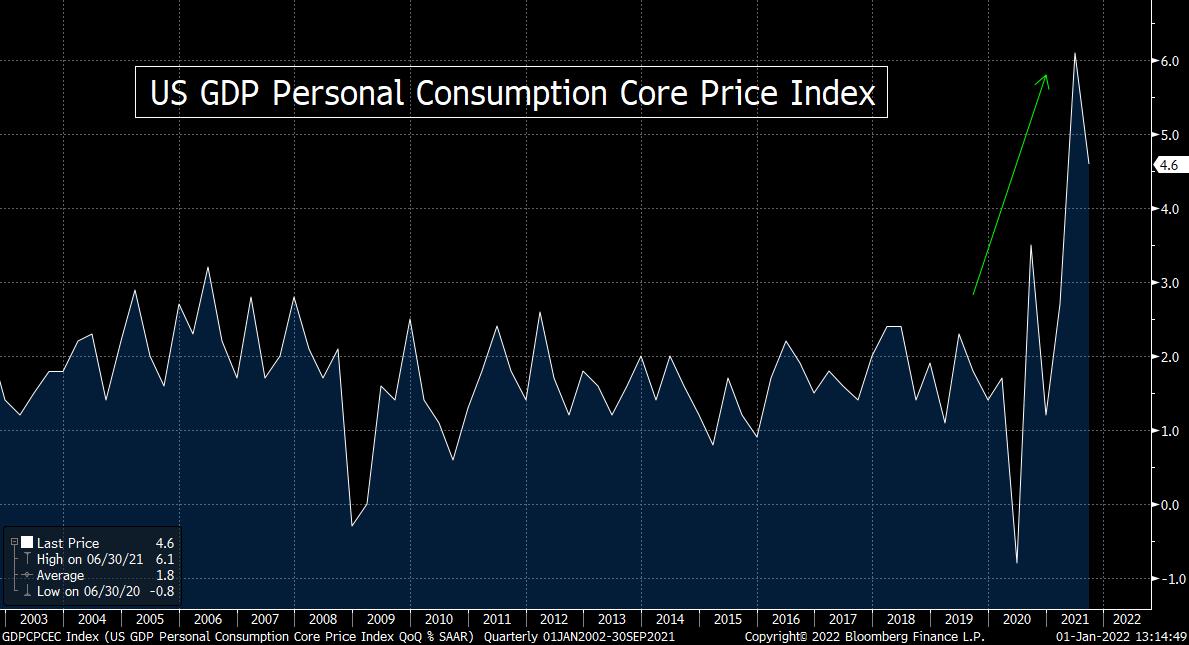

Not only are wage pressures likely to persist, but just look at the 20 year chart on the PCE personal consumption price index. It has skyrocketed this year. As we have stated several times in the past, we expect inflation to level off at a lower level than its 2021/22 peak going forward, but given the wage inflation pressures that are likely to persist, we still believe they’ll stabilize at a much higher rate than anything we’ve seen in decades.

Having said all this, long-term rates have definitely been subdued recently. A lot of this had to do with a couple of “flight to safety” moves we saw in December…when the stock market go hit hard. (First, it was the rise in the omicron variant in early December…and then it was the confirmation that the Fed is going to be much more hawkish going forward in mid-December.) …..Therefore, the technical picture is not indicating that a big breakout move in long-term rates is imminent. Instead, we’ll be watching the “symmetrical triangle” pattern that has developed in the 10yr yield. A break above the 1.7% level would take it out of hat pattern…and signal that higher rates are quite likely. However, it will take a move above the 2021 highs of 1.75% to confirm the breakout. Therefore, these are the levels investors should be keeping an eye on over the coming weeks and months. (Second chart below.)

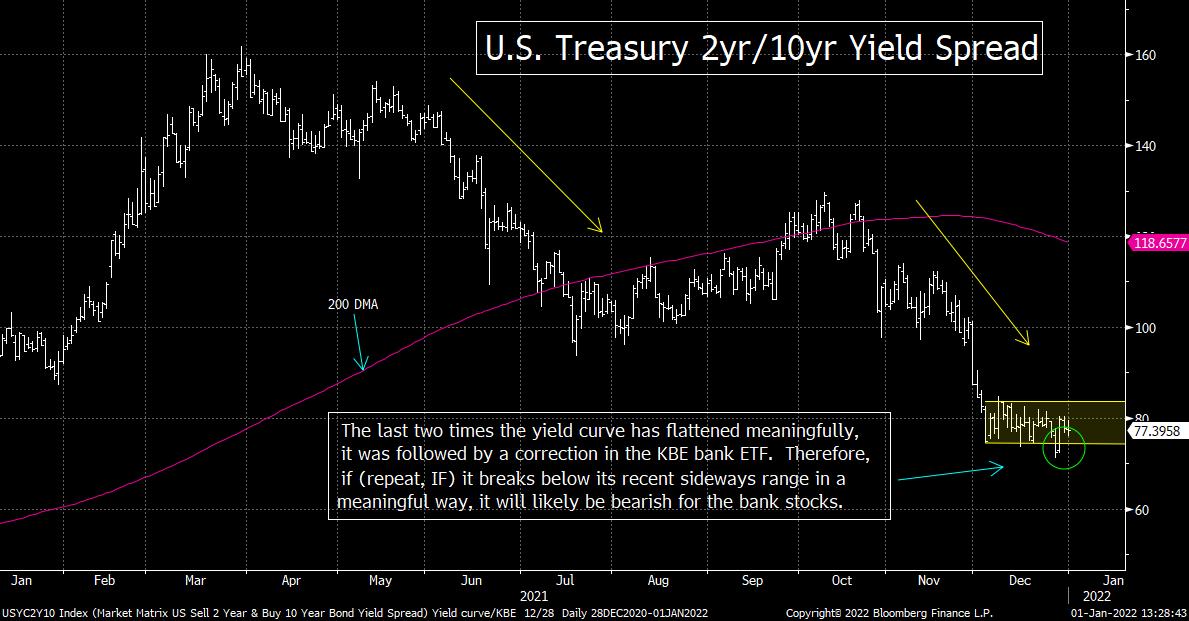

4a) It was a great year for the bank stocks…as the KBE bank index rallied over 30%. However, most of that rally came in the first few months of the year. Since March, it has bounced around in a wide range…and we worry that if the yield curve the group could have a tough start to 2022 (even though we like the group longer-term).

We turned extremely bullish on the bank stocks 15 months ago (in October of 2020)…and the group has seen an outstanding since then. The KBE bank ETF and the KRE regional bank ETF have both rallied over 90% since we turned bullish on the group. However, most of that rally came in the first six months of that move. Since March, the group has bounced around in a rather large range, but it’s still pretty much where it was in March.

We are starting to worry about this group over the short/intermediate-term…even though we still like it on a long-term basis.

First of all, the yield on the 10yr note remains below its 2021 highs (as we just highlighted). The correlation between the yield on the 10yr note and the bank stocks has been strong this year, so if those yields do not rise, it could cause the group to lag going forwared.

Second (and more importantly), the yield curve has begun to flatten once again. In fact, the 2yr/10yr yield spread has fallen to its lowest level of the year this morning (of just 73 basis points). This spread tightened (flattened) considerably in late November and the first week of December, but it stabilized at that point…and traded in sideways range for the past two weeks. However, it is close to breaking below that short-term sideways range as we move into 2022. Therefore, if this flattening move picks-up any steam again, it would indicate that the yield curve is going to see an even further flattening move as we head into the New Year.

The yield curve has been a better indicator for the banks stocks this year than just the yield on the 10yr note, so if (repeat, IF) we see another “flattening leg” in the yield curve, it’s something investors need to keep a close eye on. (When the curve flattened form May-June…and then again in November and December…the KBE saw declines of 15% and 10% respectively)…..It might sound weird that we’re calling for higher long-term interest rates…and at the same time, we’re worried about a flatter yield curve. However, history tells us that the curve does tend to flatten initially when the Fed starts to tighten. Also, if short-term rates are rising faster than long-term rates, the curve can still flatten if long-term yields are rising. Besides, as we said above, it still might be a little while before long-term rates breakout to the upside.

The bank sector has been one that has been highly touted around Wall Street in recent months, but the KBE actually stands at the same level it did in March. (Actually, slightly below its March highs.) This compares to the S&P 500…which has rallied more than 20% since its own March highs. Therefore, investors need to be careful about chasing this group as we move into 2022…ESPECIALLY if the yield curve does indeed continue to flatten.

In other words, we still like the bank stocks longer-term, but the might struggle in the weeks ahead…and thus we’re going to work with a more cautious stance on the bank stocks for the time being.

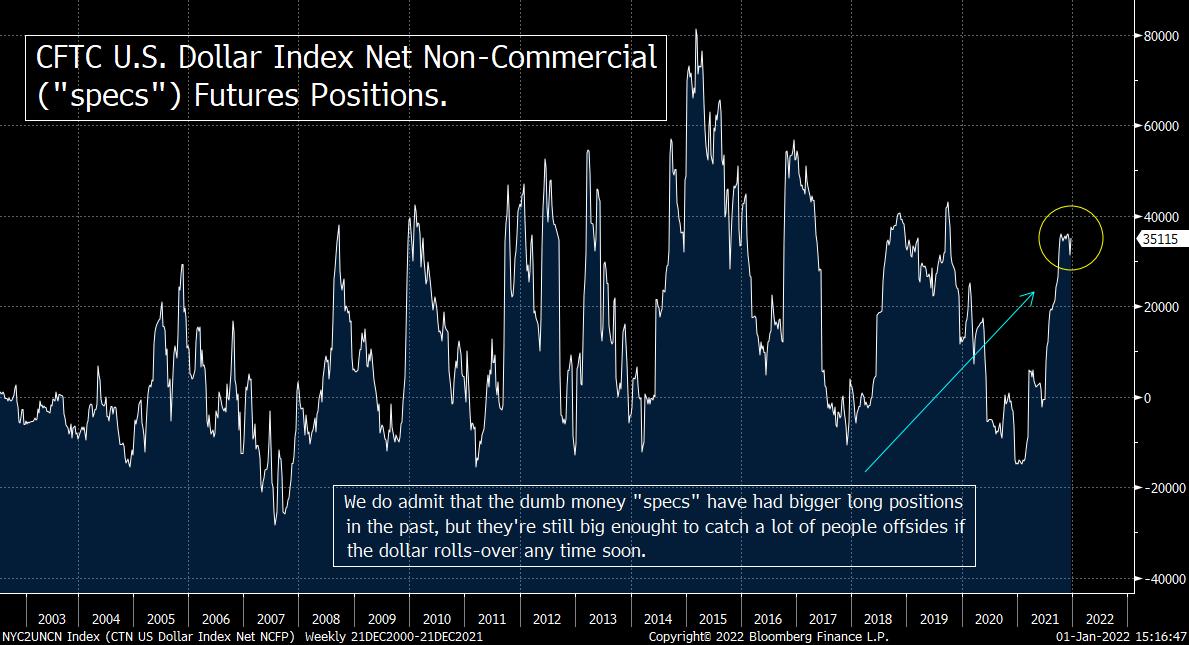

5) The rally in the dollar for the six months from late May until late November was a very strong one. However, it has flattened out over the past month. The positioning and the technical condition is flashing a yellow warning signal right now. If the dollar falls early in the New Year, that warning signal will shift from a yellow one to a red one.

The DXY dollar index has made a series of “higher-lows” and “higher-highs” since late May, so its rally has certainly been a strong/consistent one over the past six months. That said, the rally lost steam about a month ago…and its rise has flattened out over the past four weeks. This is not a problem yet. It could merely be a nice “sideways correction” before it regains its upside momentum. Therefore, we don’t want to raise any warning flags just yet.

However, the “long dollar” trade has become quite crowded during this rally…and it now reached a level where a top in the greenback frequently occurs. Looking at the COT data (Commitment of Traders), it shows that the dumb money speculators (“specs”) have a very large long position in the dollar…and the smart money (the “commercials”) have a rather large short position…..We do acknowledge that these positions are not at the most extreme levels we have seen in the last decade, BUT they are rather close to levels that have been followed by significant reversals in the dollar over the past 10 years. Therefore, we’ll be watching the DXY index very closely as we move through the early weeks of the New Year.

Since the “positioning” has reached even more extreme levels than it stands right now…and thus could become more extreme in Q1, we’ll be watching to see which way the DXY breaks-out of its recent 1-month sideways range. Needless to day, if it breaks above that range (at 97), it’s going to be bullish for the dollar and signal that it still has a little left in its current rally. However, if it breaks below that range (at about 95.50), it’s going to raise a big yellow warning flag in our minds. It closed very close to that level on Friday, so this could become an issue very quickly in the New Year.

The next level we’ll be watching is the 95 level…because that’s where the trend-line from the May lows comes-in. Any meaningful break below that line would change any yellow flag…into a red one…….We DO NEED to note, however, that the trend-line is rising. Therefore, the level we’ll be watching will rise along with it. In other words, by mid-January, that very important support line will be at 95.15…and by the end of January, it will be up near 95.50.

One final item that we’ll be watching is the weekly MACD chart on the DXY. It has gotten close to a negative cross during its recent sideways move, so if it breaks below its sideways range…at the same time it sees a negative cross on its weekly MACD chart…it’s going indicate a key change in momentum.

In other words, there is no question that some cracks are showing up in the rally in the U.S. dollar, BUT we’re going to have to see it actually begin to breakdown before we can raise any warning flags. Thankfully, we have some key indicators that should tell us if the trend is changing…rather early in that transition. Needless to say, a change in trend for the green back could/should have important implications for other asset classes…like commodities and emerging markets.

6) We remain bullish on the energy stocks. Even though they are no longer incredibly cheap and wildly under-owned (like they were when we first turned bullish on the sector in October of 2020), but they’re still cheap and under-owned on an historical basis. More importantly, the supply/demand equation continues to look favorable for crude oil.

If the dollar does indeed break down as we alluded to as a possibility in the previous point, it should be bullish for commodities, including crude oil. However, although the inverse correlation between the dollar and crude oil is a good one, it’s not as always strong as it is with other commodities. Therefore, we’d like to speak to the fundamental side of our bullish argument first.

We believe that the supply/demand equation favors higher WTI crude oil prices. On the supply side of the equation, global spending on oil & gas projects is well below the pre-pandemic levels of $520 billion. We are all in favor of moving away from fossil fuels, but it cannot be done overnight. We need to continue to keep the production side strong in fossil fuels through the rest of the decade…and right now, the money is not there to do this….as the U.S. and other producers have cut back on this spending significantly.

On the demand side of things, we have already reached pre-pandemic levels in terms of crude oil demand…and the IEA says that demand will remain with 5% of pre-pandemic levels through the rest of the decade! Again, we all want to move away from fossil fuels as quickly as possible, but it will still take more than a decade to achieve this goal. Therefore, even though many producers are planning on increasing production next year, it will not be enough to meet demand…especially since the output from many existing oil fields is declining.

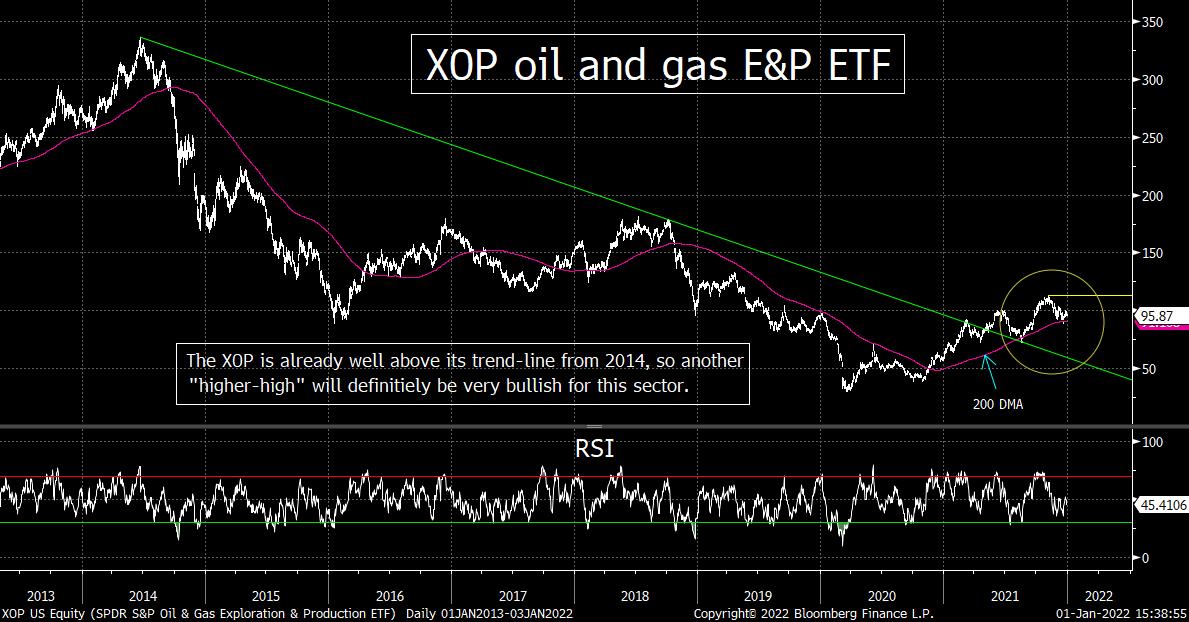

Therefore, whether the dollar declines or not next year, the supply/demand equation should remain quite bullish for crude oil….On the technical side of things, we love the fact that WTI saw a “golden cross” on its weekly chart (something we highlighted several weeks ago. This could be quite important because the XLE energy stock ETF is testing its trend-line going all the way back to 2014! Therefore, if it can break above this trend-line, it’s going to be very bullish for the energy stocks. Right now, we are watching the $60 level on the XLE. A break above that level not only give it another “higher-high” (above its Oct/Nov highs), but it will also take it above its 8-year trend-line. THAT will be very bullish (if it takes place).

As for the XOP oil and gas E&P ETF, it has already broken above its 8-year trend-line, so when you combine this…with the “golden cross” in the underlying commodity (plus a possible change in trend for the dollar)…you have many reasons to think that the bull market for the energy sector will continue well into 2022 (and likely beyond).

7) The semiconductor stocks saw a VERY nice rally in the 4th quarter of 2021. Demand remains very strong and thus many investors are looking for further gains in 2022. We would note, however, that several cracks are forming in the SMH semiconductor ETF, so if the group rolls-over early in the New Year (which we admit is a BIG if)….it would raise a surprising yellow warning flag for this group.

The chip stocks had an excellent 2021…with the SMH semiconductor ETF rising over 41%. Half of that advance came in the 4th quarter, so unlike some groups (like the industrials), they did not stall-out midway through the year. However, we do need to note that the action in the SMH over the last few weeks of the year raised some questions about whether the rally will continue as we move into 2022.

Since mid/late November, the rally in the SMH became a very choppy one. It saw three different declines of more than 4% and one of over 6%. On the

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464