Morning Comment: What are the NY Yankees telling us?

When we left the office yesterday, we thought we’d be starting this morning’s piece with a joke about NY Yankees. We were going to say that the story about several Yankees testing positive was completely made up…because they didn’t want to get swept by the Red Sox again! However, the more we thought about it, the more we realized that the new variant of the virus is nothing to joke about. There’s no question that the Delta variant is creating new problems in many parts of the world (and is wreaking havoc in places like Melbourne, Australia).

No, we’re not saying that we are going to return to the kind of lockdowns that we saw in 2020, but it could still be enough to have an impact on economic growth in the second half of the year. Therefore, one of the reasons that yields just might be due to concerns over a slowdown in growth.

HOWEVER, we believe that if investors are buying Treasuries over concerns about growth, they’re making a big mistake. First of all, most of the recent decline in yields has been due to positioning, not concerns over growth. Second, slower growth is not going to be a reason for the Fed to avoid tapering back on their bond purchases. If the pace of economic growth slows due to the Delta variant, the level of growth should still be fine. In other words, we will still be in a situation where the economy (and the markets) is no longer in an emergency situation, so the Fed will still have to taper-back on their emergency levels of stimulus. (Of course, if the Delta variant becomes a major killer…and the economy DOES shut-down again…all bets are off.)

What we’re saying is the same thing we’ve been saying for a while now. The Fed is not “data dependent.” Their decision on when to taper has little to do with economic data (employment data or otherwise). They’re only saying that they’re data dependent so that we don’t get the reaction to their upcoming plans to “taper” all at once. The rise in long-term rates is coming later this year because the demand side of the supply/demand equation is going to change. The Fed is going to buyer fewer bonds. That’s going to cause price to fall…and yields to rise. Therefore, those who believe today’s yield levels are an indication of how things will playout over the rest of 2021 are way off base in our opinion.

Moving back to the stock market, it saw a mild pull-back yesterday…as the tech stocks rolled-over in a meaningful way. We don’t want to overstate this move in the tech sector (at least not yet). The XLK tech ETF only fell 0 .82%...and that decline came from an all-time high. Thus, we are a long way from waving a major warning flag on the tech stocks in general. However, we did see some steep declines in the stocks we highlighted yesterday morning. (The ones we said have become ripe for a pull back.) Taiwan Semiconductor (TSM) fell 5.7% and Nvidia (NVDA) declined 4.4%. These moves weighed quite heavily on the SMH… as TSM & NVDA make up 25% of the SMH…and so the SMH fell 2.7%. (We’d also note that the other ETF we highlighted yesterday…ARKK…also took it on the chin yesterday by falling 1.5%.)

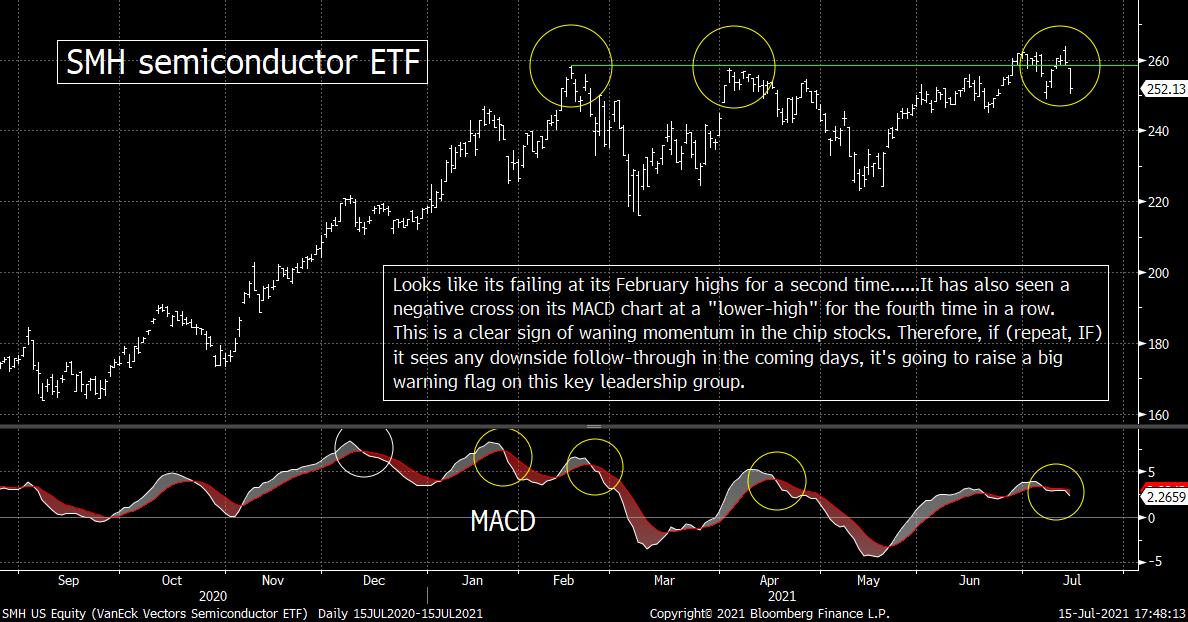

This means that the SMH failed to break above its February highs in a meaningful way once again. The first time it “failed” was in April…and that was followed by a 13% decline in the chip stocks’ ETF over the next six weeks. Of course, one day does not make a change in trend, so we don’t want to try to say that yesterday’s action tells us that we’re definitely about to see a correction in the chip stocks. We’ll have to see if the SMH sees any downside follow through…either today or next week.

If (repeat, IF) the SMH does indeed see some downside follow-through before long, it’s going to be quite negative on a technical basis for the semis. Looking at the chart below, you can see that the SMH has just experienced a negative cross on its MACD chart. That negative cross has taken place at a “lower-high” for the fourth time in a row! This is a sign that tells us that as the SMH has been trading in a sideways pattern for many months, the momentum beneath the surface has been waning. In other words, the divergence between its price chart and its MACD chart on the SMH is a warning flag for the semis…and thus if we see any downside follow-through over the next week or two, it’s going to cause our concerns for this group to grow significantly.

Matthew J. Maley

Chief Market Strategist

Miller Tabak + Co., LLC

Founder, The Maley Report

TheMaleyReport.com

275 Grove St. Suite 2-400

Newton, MA 02466

617-663-5381

Although the information contained in this report (not including disclosures contained herein) has been obtained from sources we believe to be reliable, the accuracy and completeness of such information and the opinions expressed herein cannot be guaranteed. This report is for informational purposes only and under no circumstances is it to be construed as an offer to sell, or a solicitation to buy, any security. Any recommendation contained in this report may not be appropriate for all investors. Trading options is not suitable for all investors and may involve risk of loss. Additional information is available upon request or by contacting us at Miller Tabak + Co., LLC, 200 Park Ave. Suite 1700, New York, NY 10166.

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464