THE WEEKLY TOP 10

Just a reminder, we are only putting out one “version” each weekend now. The first paragraph will be in bold letters and will serve as the old “Short Version” of the piece (usually a condensed review of the “Long Version.”) This seems to be the preferred way to do it based on the feed back we’ve received so far.....Thank you.

THE WEEKLY TOP 10

Table of Contents:

1) A big warning shot across the bow last week. More de-leveraging to come.

2) It has been liquidity, not “margin expansion” that has fueled the market for years.

2a) Earnings are less important right now, but that will change quickly.

3) A further rally in the dollar should create another round of de-leveraging.

4) Still keeping our powder dry (for now) on our three favorite groups.

5) China’s stock market is at an important technical juncture.

6) The European bank index needs to hold its key support level.

7) The near-term support/resistance levels for Bitcoin are easy & well defined.

8) Congress is filled with hypocrites (on both sides of the aisle).

9) Support levels for the S&P 500, the QQQ and the IWM.

10) Summary of our current stance. (Corrections are normal...embrace them!)

Long (and only) Version:

1) Despite the fact that last week was the biggest week for earnings during this earnings season, that subject took a back seat to the GameStop phenomenon and the Robinhood traders. Traditional long-term investors probably don’t like the lack of focus on earnings, but we believe that it was correct that earnings took a back seat last week. HOWEVER, the reason we believe the GameStop/Robinhood issue was more important is a lot different than most people might think. The real reason why it was more important is because it represented an important warning shot across the bow for the stock market.

We got an important warning shot across the bow last week for leveraged investors with the short-squeeze on several highly shorted stocks. Since there is a record amount of leverage in the system, it was ALSO an important warning shot for all investors AND the entire stock market. Like other warning shots we’ve seen over the years in the stock market, this does not necessarily mean that the broad market is about to roll-over in a significant way immediately. However, it DOES signal that odds that we’ll see a deep correction at some point in the coming weeks/months are much higher than most investors realize...and therefore they should adjust their portfolios accordingly.

The level of margin debt has reached an all time record high, so there is no question that there is a lot of leverage in the markets today. The problem is that the amount of leverage in the small number of stocks that got squeezed last week pales in comparison to the level of leverage on the long side of the stock market right now. Therefore, the thing that worries us the most is that the “unwinding of leverage” on the short side...is already leading to the “unwinding of leverage” on the long side...for the simple reason that these leverage investors cannot meet their margin calls by covering those stocks at such high levels. This means that the “unwinding of leverage” on the short side is spilling over to the long side of the market. Thus we’re getting the “unwinding of leverage” from both sides.

It doesn’t end there! We’ve also see firms like Robinhood shore up their own situation by tapping lines of credit. When firms need to make moves like that, it leads to MORE “unwinding of leverage” in the system. Some of it is “forced.” However some of it is merely investors looking at the situation...and seeing that the system is so incredibly leveraged that they need to lower their own levels of leverage...in case things start to snowball. This can sometimes lead to a self-fulfilling prophecy that leads to a major decline. Other times, it can lead to a less-than-major decline, but it still usually leads to at least SOME more de-leveraging by the investment community. This what we’re looking for going forward.

In other words, even if don’t see another round of short squeezes next week, we could easily still see a decent amount of de-leveraging around Wall Street (and around the globe) going forward. Either way, we’re starting to see the signs that the massive levels of excess leverage that has built-up in the system since last spring is going to be unwound to the degree that will (at the very least) create some headwinds for the stock market and other risk assets for more than just a few days.

This all may sound a bit crazy to you...to think that the short positions in the stocks of couple of small companies with lousy prospects can be the catalyst for a deep correction in the stock market. Well, it’s not the action in these specific (highly shorted) stocks that worries us. IT’S THE FACT THAT THEIR WILD MOVES ARE EXPOSING THE MASSIVE LEVELS OF LEVERAGE IN THE SYSTEM...as well as exposing a lot of new inexperienced investors to what can happen when even a little bit of that leverage if “forced” to be unwound.

“De-leveraging”...whether it be “forced buying” or “forced selling”...can (and frequently does) feed on itself. Thus it can QUICKLY turn a minor de-leveraging process into a much more pronounced one when the levels of leverage are abnormally high......No this does not mean that last week’s action will turn the recent decline into an immediate rout. However the short squeeze in GME did cause a major (and well respected) hedge fund (Melvin Capital) to get bailed out...and those of us who remember when a few highly leveraged hedge funds (at Bear Sterns) went belly-up in 2007, it was a precursor for things to come.

When bailouts take place at bottoms, they tend to signal that the market has become “washed-out” and poised for a significant bounce. HOWEVER, when a bailout takes place at/near a top, they tend to signal that a lot of other leveraged entities are in big trouble as well...and bailout tends to be a precursor of more de-leveraging to come...rather than an important bottom. (In other words, the bailouts at tops tend to be done to protect existing leveraged positions...while bailouts at bottoms are done to create big future gains for the buyers.)

2) Then again, maybe stocks like GME, AMC, BBBY and other highly shorted stocks SHOULD be trading at this weekend’s lofty levels! Maybe what has really been happening to these stock over the past week or so...is the same thing that has been taking place in the rest of the market for most of the past 10-12 years. Maybe these moves are totally justified because these stocks are merely rallying due to “multiple expansion.”

Needless to say, that last comment was totally ridiculous. “Multiple expansion” is not a reason for a stock to rally. It’s just an excuse investors use to justify buying and holding a stock that has become very expensive........No, it’s not as ridiculous as saying that a lot of other assets have rallied strongly in recent years due to multiple expansion, but it’s a lot closer to being just as ridiculous than most pundits will admit.

In other words, the real reason why stocks like GME, AMC, and BBBY have really rallied so strongly recently is because there has been a short squeeze. Everybody realizes this...and accepts this. However, most pundits are notwilling to realize or accept that the real reason why many more stocks (and other risk assets) have been rallying strongly for years. They claim it has taken place because interest rates have fallen and thus higher multiples are justified...when the real reason for much of the rally has been due to central bank liquidity.

Of course, the two go hand-in-hand. The artificial liquidity that pushed into the system by the central banks through the buying of long-term bonds (QE)...push long-term interest rates to artificially low levels. However, we don’t believe that THIS is what allows stocks (and other assets) to move higher. Instead, we believe it’s the fact that the excess liquidity...HAS to find a home...and THAT creates the upward moves. In other words, if interest rates were to stay low without artificial stimulus...and instead, stayed low due to a very poor economy...we believe that the stock market would fall out of bed...as investors would no longer have the excess liquidity to buy risk assets...no matter HOW LOW interest rates fell.

Another way to say this is to say that we strongly believe that if long-term interest rates were allowed to trade freely...instead of being constantly manipulated through QE programs...and they still stayed at historically low levels (and even fell further), the stock market’s multiple would NOT continue to expand...or even hold-up............That’s right, if interest rates stayed low due to a lousy economy...and there was no excess liquidity looking around for a home...the stock market would dive (even though rates were at an ultra low levels).......So, without the excess liquidity, instead of expanding or holding at high levels, the stock market’s multiple would contract faster than guy’s family jewels when he jumps into a cold lake. (It would give a whole new meaning to the term “shrinkage”!!!)

2a) With all the talk surrounding the GameStop phenomenon, earnings season got lost in the sauce last week...even though it was the heaviest week for earnings of the season. Then again, this earnings season was never going to be as important as they usually are at the beginning of a year. What we always care about when Q4 earnings come-out, is the guidance the companies give us for the new year. However, we have known for a while now that there wasn’t going to be a lot of guidance forthcoming this time around. To many companies don’t know enough about their 2021 prospects...because they don’t know how fact the economic lock-downs will be reversed.

Don’t get us wrong, earnings are still VERY important, but they’re much more important for the individual stocks during this earnings season. Without a lot of guidance, it will take time before we get a good reading about whether today’s stock market is just very over-valued compared to 2021 earnings...or seriously over-valued.....We should have a little bit of a better idea once the entire earnings season is over, but for now, it’s just the individual stocks that seem to move on these reports.

Sure, on the bullish side of things, it’s great that more companies than usual are beating estimates...but the majority of companies always beat their estimates, so it’s hard to get overly excited on that data. On the bearish side, we’d note that it’s disappointing that a lot of stocks are not responding well to better-than-expected earnings reports.

Before last week, A LOT of pundits were saying that earnings estimates were way too low on the street. That’s great to hear, but we think it’s going to take another few weeks (and probably into March) before we get a true understanding of what the full year 2021 earnings are going to be. Heck, they might even be better than even the most bullish estimates, but either way, it’s going to take more time before we know for sure in our humble opinion. Therefore, the earnings picture will probably continue to take a back seat to other issues...at least for a little while longer.

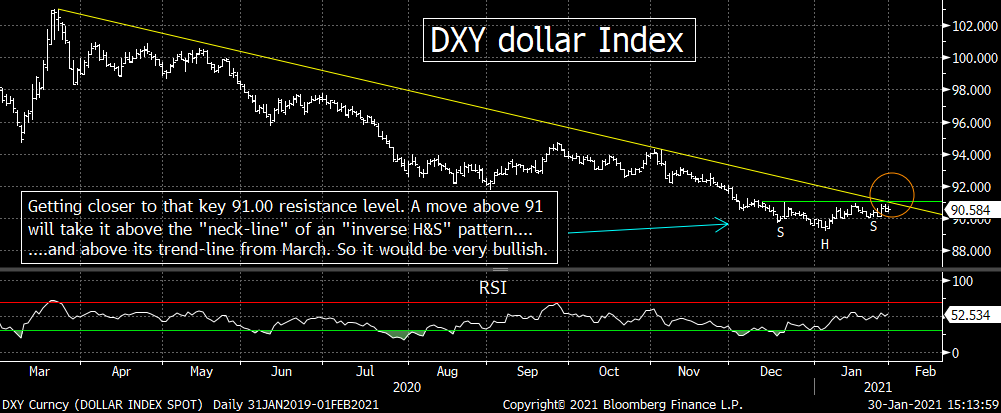

3) We still believe that the currency market should hold the key for what happens in many (most) markets over the coming weeks and months. The U.S. dollar is moving closer to its KEY resistance level (and the Aussi dollar is closing-in on its key support level). If these levels are broken in any compelling way, it should catch a lot of investors offsides...which, in turn, should cause another increase in volatility in many different markets. (This will be especially true if highly leveraged players are “forced” to buyback the dollar and sell the Aussi dollar.)

We’ve been saying for a couple of weeks now the U.S. dollar had become extremely oversold, over-hated, and over-shorted...and thus had become ripe for a “tradable” bounce...even though the fundamental outlook for the greenback points to a lower dollar over the long-term. Sure enough, the dollar has been gradually climbing since early January...and it’s now getting quite close to the very important resistance level of 91.00 on the DXY dollar index.

A meaningful move above 91 would take it above its trend-line from March...AND take it above the “neck-line” of an “inverse head & shoulders” pattern. Therefore, we believe that kind of breakout would cause many momentum players to reverse their current positions...and THAT should create the kind of counter-trend move that will last at least several weeks.

As for the Aussi dollar (the AUD), we do admit that is still quite close to its early January highs. However, it has fallen a little bit...and we’d note that its weekly RSI chart had reached the same overbought condition that it reached just before it saw a multi-week decline in 2020, 2018, 2017, 2011, 2010, and 2009.

We’ll be watching the 0.7750 level on the AUD vs. the U.S. dollar...which is just below its current level. Any material break below that level will take it below its trend-line from March. Given that the Aussi dollar has been a popular currency in the “carry trade,” any meaningful decline in the dollar will not be a good sign for amount of net liquidity in the system available to push risk assets higher.

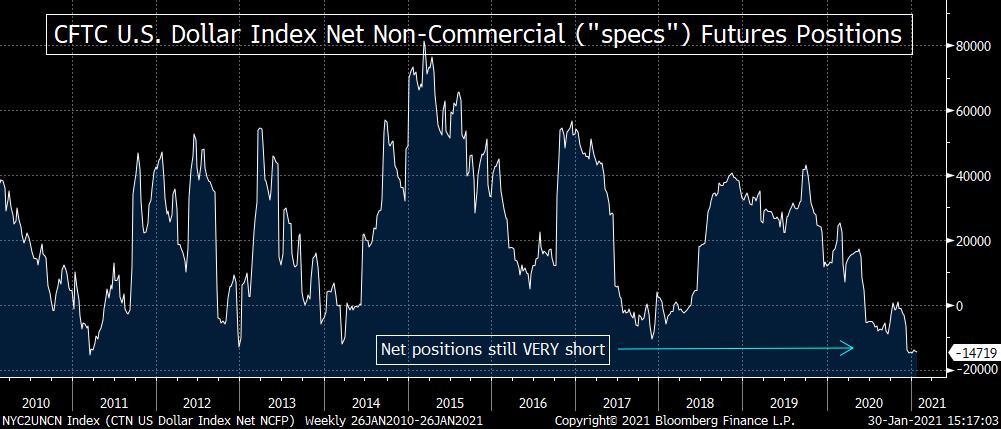

The thing that worries us the most about these moves is that they’re coming at a time when many investors are ALREADY being “forced” to unwind their leverage in other markets. If the very crowded “short dollar” trade starts to get reversed while these other de-leveraging processes are playing out (or if it happens in their immediate aftermath), it’s going to accelerate the deleveraging process. This is something that FEW investors are prepared for right now.

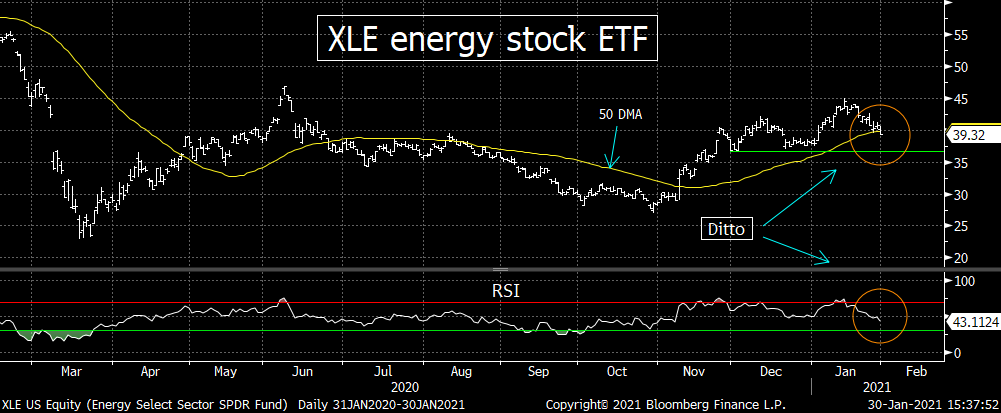

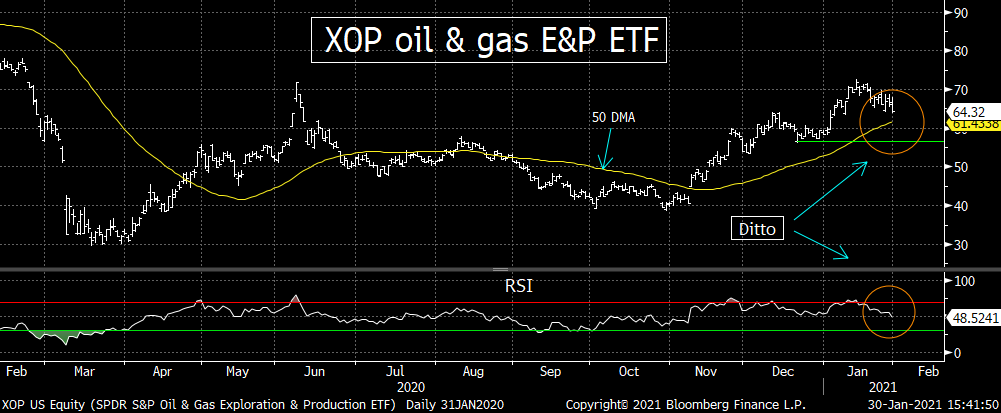

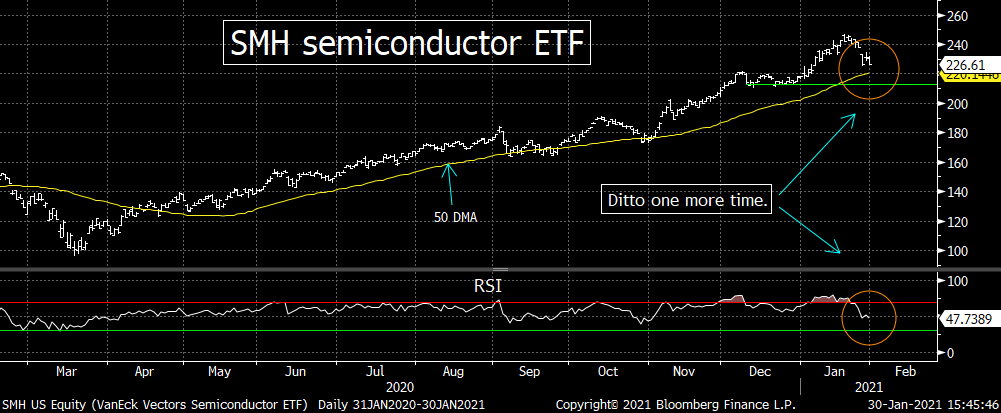

4) We had been very bullish on the stock market over the last four months of last year and into early this year, but we had been particularly bullish on the bank stocks, chip stocks, & energy stocks. HOWEVER, we changed our tune two weeks ago on all three of these groups...on a short-term basis...and that strategy has worked-out very, very well. Due to the fact that we think the broad market can fall further, we’re going to stay away from these groups for a bit longer.

Even before the broad stock market rolled-over, we warned that all three of our favorite groups...banking, semis, energy...had become very overbought on a short-term basis. We also noted that the bond market had become oversold (& thus the 10yr yield had become overbought)...and the dollar had become deeply oversold. Therefore they were ripe for counter-trend moves...which would be negative for the bank and energy names......Given these developments, we said that traders could take a few chips off the table...and longer-term investors should avoid chasing them up at their early-January levels. (Our caution on the semis dealt solely with the overbought condition of the SMH...and several individual names like TSM & MU.)

Sure enough, the bank & energy names rolled over almost immediately...and the semis topped-out when the broad market did (a week or so later). The KBE bank ETF has declined more than 9%., the XLE energy and the XOP oil & gas ETF’s have both fallen about 11%...and the SMH semiconductor ETF has given back almost 8% from its January highs (and -6% from when we made that cautious call). Therefore, these calls have worked-out exceedingly well.

Okay, that’s great...but what next? Well, since we’re concerned about the broad market, we think they will all see some more weakness over the coming weeks. For all of these ETF’s, the 50 DMA is the first support level to keep an eye on. (Actually, the XLE is already touching that moving average.) However, we’re going to use the 4th quarter lows in each of these ETFs as the levels we’ll be looking to start adding to positions in these groups once again. (We do what to say that we think it’s fine to start nibbling in these groups very lightly right now...since we like their prospects over the entire year this year. However, we think any buying should be done in a very gradual manner...while waiting for the baby to be thrown-out with the bathwater...before we get aggressive.)

For KBE, the we’ll be looking at the December lows of 40.50...for the SMH, it’s 212.50...for the XLE, its $36.75 & for the XOP it’s $57.25. (We might get more aggressive at $59.50 on the XOP...which is a Fibonacci 38.2% retracement of the rally from October/November lows. However, we’ll want to see how the broad market is trading if/when the XOP reaches that level. If the broad market looks dicey, we’ll wait for those late December lows of $57.50 that we mentioned first.)

Again, we like these groups on a longer-term basis...and we think they will outperform the broad stock market for the rest of the year. However, given our concerns about the broad stock market over the coming weeks, we’re going to lay in the weeds for a little bit longer. If the market does see a more significant round of “forced selling,” it should provide a GREAT opportunity to buy them. Therefore, we might not get overly aggressive if the above-mentioned support levels are hit, but we’ll get aggressive at some point going forward.......In other words, the key right now it to keep the powder dry. We will definitely let you know when we think it’s time to jump back-in with both feet. However, we still wanted to provide you with the general guidelines we’re looking at right now for each group.

5) We’ve spent a lot of time recently talking about China...and the U.S./China relations (especially when it comes to Taiwan), but we’d like to shift gears and look at the technical aspect of China’s stock market...because it is testing a VERY important resistance level. Therefore, whichever way it breaks over the coming weeks could/should be important for that stock market for many months...and maybe even over the rest of the year.

First of all, after a 36% rally off the March lows, China’s Shanghai Index is now testing its early 2018 highs. So if it can move meaningfully above those 2018 highs...and thus give it a very important “higher-high,” it’s going to be very bullish for the Shanghai index on a technical basis.

More importantly for U.S. investors, the FXI iShares China Large-Cap ETF bumped up against its highs from 2015 and 2018 earlier this month. It did pull-back last week, but if it can break above that “double-top” high in any significant way over the coming weeks, it’s going to be VERY bullish for the FXI!!! HOWEVER, if it fails to breakout...and last week’s decline turns into a pronounced drop...it could/should be a very negative development. The last two “failures” up at these levels were followed by declines of 46% and 29% respectively...so things could get ugly if the Chinese stock market fails to breakout once again.

On the fundamental side of things, we keep hearing how China is coming out of the global pandemic quite nicely and that they’ll lead the global economy out of the historic shut-down of 2020. However, we’d also note that the IMF actually lowered its estimates for growth in China (while raising it for the U.S. and other parts of the world). Don’t get us wrong, they only lowered it from 8.2% growth to 8.1%, so it was not a dramatic move by any means.

In other words, China’s stock market looks good...and if the Shanghai Index and the FXI can break above their all-important resistance levels in a significant way, it’s going to be very bullish for that market. However, as always, we HAVE to wait for that breakout to take place...because history has told us that a “failure” at this key resistance level can turn the situation 180 degrees very, very quickly.

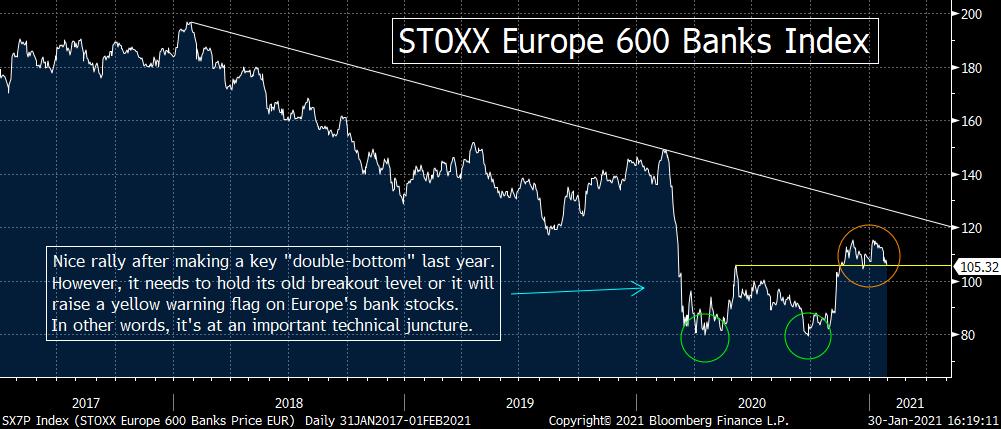

6) As much as we like the U.S. bank stocks on a longer-term basis (even though we’re taking a “breather” from them right now), we’re not as sure about the European banks. The saw a very strong rally in November, the European banks did not see any upside follow-through in December & early January like the U.S. banks saw. Now, they’ve begun to roll-over, so if they see any further weakness, it will raise a big warning flag on this group from across the pond.

The STOXX Europe Banks Index broke-out of a seven month sideways range in November...which seem to give the group a lot more upside potential on a technical basis. This was particularly true since the “higher-high” the index made had come right after it had made a very nice “double-bottom” low over the summer. In fact, it followed that “higher-high”...with a “higher-low” in late December...so the group’s prospects looked quite good.

Having highlighted these bullish technical developments from last year, we do need to point out that the key European bank index was unable to make another “higher-high” in January...and instead seems to have made a minor “double-top.” Therefore, we’ll be watching an important support level next week to see if it can hold. If it can’t...and breaks below this key support level, it will quickly raise some more concerns about the banking sector from across the pond.

The level we’re talking about is the 104.50 level. That was the June highs...and it was the top of the multi-month sideways range we referred to above...and thus it was the “old resistance” level. As we frequently say, “old resistance” becomes “new support”...and sure enough, this European bank index fell back to that “new support” level in December...and held! However, it is now getting very close to retesting that level once again. Therefore, if (repeat, IF) it breaks below that level in any compelling manner, it will be a negative development on a technical basis.

One last point about this chart. Even though the STOXX Europe Banks Index was able to break above a sideways range two months ago, it was still below its trend-line from the early 2018 highs. Thus a break-down from current levels would signal that the European banks still have a lot of work to do before they can reverse their long-term downward sloping trend. With pandemic issues still stifling Europe, we suppose the inability of this group to give us a more compelling break-out probably shouldn’t be a surprise.

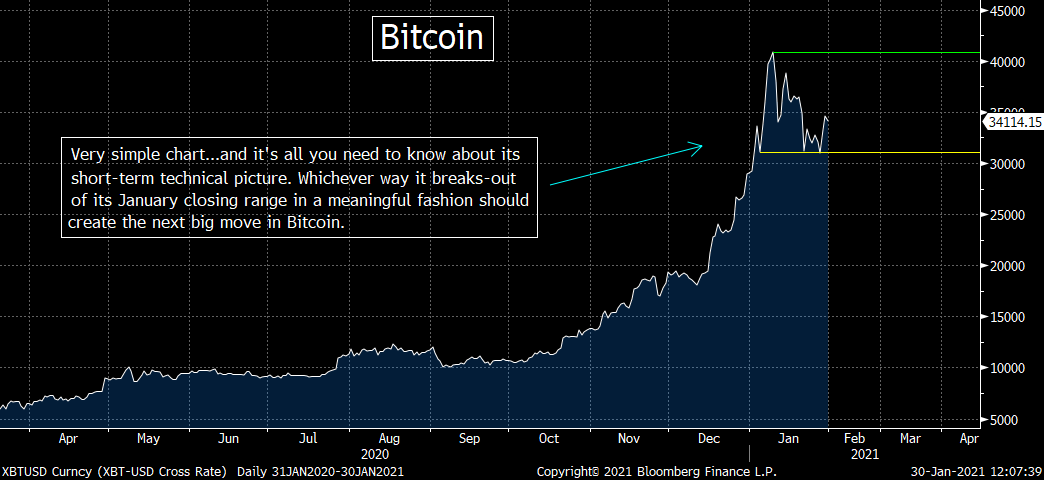

7) There are a zillion things we could talk about when it comes to Bitcoin right now, but since this is something that gets talked about and written about many times every day, we thought we’d keep it simple this weekend. (Besides, we’ve talked a lot about it in recent weeks as well.) We’ll just look at a very simple chart...because the support and resistance lines are still very simple and well defined.

The chart on Bitcoin is an easy one to decipher right now. The support level that we highlighted last weekend of just above 31,000 is still intact. That was the closing low from January 4th and January 21st...and it got RIGHT AT that level on Wednesday (the 27th)...and bounced once again. Therefore, this has become an incredibly important short-term support level for Bitcoin on a closing basis. Any meaningful break below that level (again, on a closing basis), will be quite negative...and should lead to a sharp near-term decline.......However, if the cryptocurrency were to regain the upside burst it saw Friday morning...and it can break meaningfully above its January all-time closing highs of 40,800...it will be very bullish for Bitcoin near-term.

When it comes to the short-term chart, that’s all you need to know. Anything else you hear on the near-term technical side of things in Bitcoin is just noise.

8) It is great that Senator Sherrod Brown says he’s going to hold hearings about the decision by some brokers to stop accepting certain orders on the heavily shorted stocks late last week. He says that it sure seems like the Wall Street firms changes the rules when a situation is hurting them...but they never seem to act if/when it’s hurting their customers.

We think it is great that Congress is looking into a situation where some people of power and influence might be taking advantage of the little guys...by engaging in some activities that those “little people” cannot engage in.

While they’re at it, we hope they’ll look at some other examples of when people of power and money get a much better deal than the rest of us. For instance, we hope we’ll look at the rule that says member of Congress can legally engage in many types of insider trading that is illegal for everybody else. They could also look at the reason behind why any member of Congress (who serves for more than 2 years) gets FULL medical benefits for LIFE...and it does not cost them a dime......We’re just saying it would be great if members of Congress were looking out for the little guy in ALL aspects of American life.

On a separate issue, as we said just after the election, the anti-establishment movement did not originate with Donald Trump and it will still be alive after Trump leaves office. After several firms put trading curbs on many stocks with high short interest yesterday...a move that seemed to protect the big money Wall Street players at the expense of the “little guy”...we’re even more confident that the anti-establishment movement isn’t going to go away anywhere soon.

We have to remember that MANY people who voted for Joe Biden were really voting AGAINST Donald Trump. They realize that President Biden is the absolute epitome of the “insider” ruling class...but they’re willing to give him a chance...because he’s not Trump. However, if they continue to experience what they’ve been fighting against since the financial crisis (like they did yesterday), Mr. Biden’s honeymoon might not last as long as he was hoping. (People can argue whether these firms did the right thing or not. However, many people...especially the millennials...view what took place yesterday as just another way that the establishment is screwing them.)

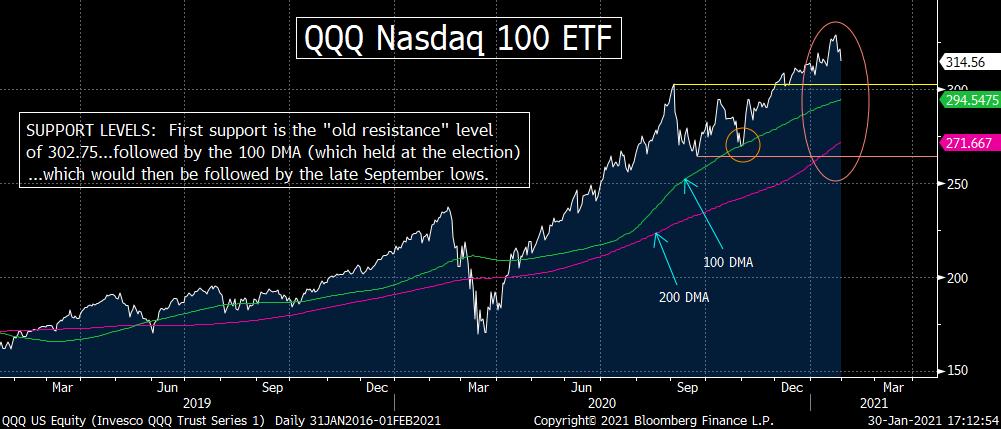

9) If the market sees some more weakness next week, we thought it would be important to cover the support levels on the S&P, the Nasdaq and the Russell 2000.....We covered the S&P in our Friday morning piece...and we’ve repeated that again this weekend. However, we have also added the support levels (and the charts) for the ETFs on the Nasdaq and Russell 2000 (the QQQ’s and the IWM).

The first support level for the S&P 500 Index is the 50 DMA. The index dipped below that line for a couple of days in September and then again in October...but it was able to regain that line rather quickly each time. So the 50 DMA should provide some initial support if the market fall further. Below that, we have the 3565 level...which was the lows on November 20th...and a 50% retracement level of the rally since the election.

If those levels don’t hold as we move through the rest of the first quarter, the next support level will be the 100 DMA of 3560. That’s the line that held in September...and then again just before the election........Of course, many people will then look at the 200 DMA of 3345 if the 100 DMA is pierced, but we actually believe that the 3233 level will be the more important level to watch. That was the lows during the 10% correction we experienced in September, so a move below that level would give us a key “lower-low.” That 3233 level is ALSO a Fibonacci 38.2% retracement of the March-January rally...so it will be a VERY important one if the market does indeed see a correction before too long.

On the QQQ, the first support level is the 302.75 level. That’s the old highs from September 2nd (and thus the breakout level from December). Since “old resistance” becomes “new support”...and since that level is also a Fibonacci 38.2% retracement of the rally from the September lows, that’s the first key level we’ll be watching......The next support level (like it is for the S&P) is the 100 DMA. That’s the line that the market bounced off of right around the election......Finally, the 264 level should be a VERY important support level if things get a little bit ugly. That’s the lows from the September correction AND its very close to a Fibonacci 38.2% retracement of the entire rally from the March lows AND it’s not far below the 200 DMA for the QQQ!

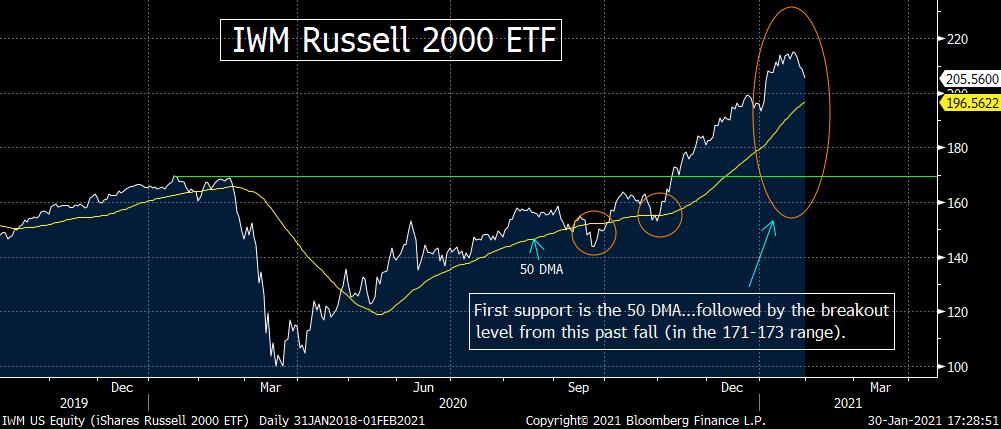

Finally, we have the IWM Russell 2000 ETF. Since this index played catch-up in recent months...and has rallied more dramatically and in more of a vertical fashion...it will likely fall a bit further on a percentage basis before its hits its own support levels. The first one is the 50 DMA of 195.50...followed by the 171-173 range. That range is where the old resistance (break-out) level comes in...as well as a Fibonacci 38.2% retracement of the entire rally from March. Any break below that level would leave it vulnerable to a quick drop down to its September lows of 143.

Having said all this, we’d also highlight that the January all-time highs are the key resistance levels for each of these indices/ETFs....and they’re all only 3%-4% above their closing prices from Friday!!!.........One last point. If these indices/ETFs were indeed to drop to the lowest support levels we just highlighted, it will mean that they had fallen 16% from its recent all-time highs (-20% for the IWM). That will be scary, BUT it will also be normal and healthy. SO IT’S SOMETHING INVESTORS SHOULD EMBRACE, NOT FEAR!!!

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464