The Weekly Top 10; June 9, 2019

THE WEEKLY TOP 10

Table of Contents:

1) Our call for a bounce worked well...but we don't think it will continue.

2) The Fed has shifted, but not enough to think they'll act before another decline in stocks.

2a) Any pre-emptive move by the Fed will be on the economy, not on the markets.

2b) A pre-emptive move after only a 7% decline will lead to a bubble going forward.

3) So of the Fed acts soon (time wise), it will only be due to a further market decline.

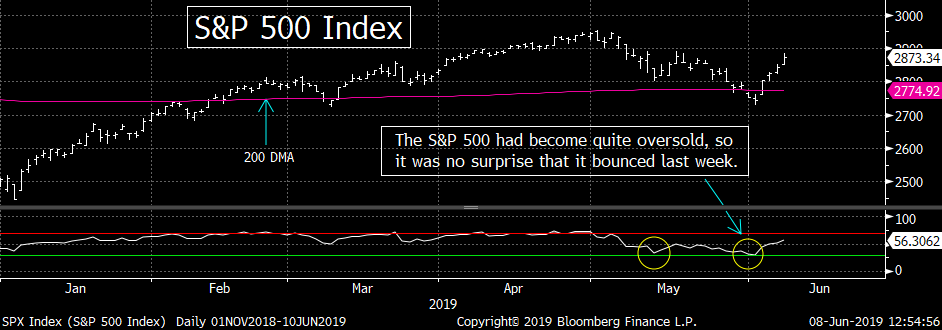

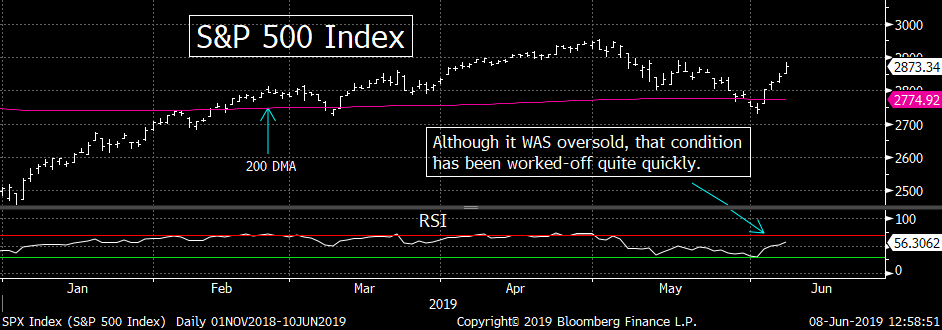

3a) There are many signs that the oversold condition has been worked-off.

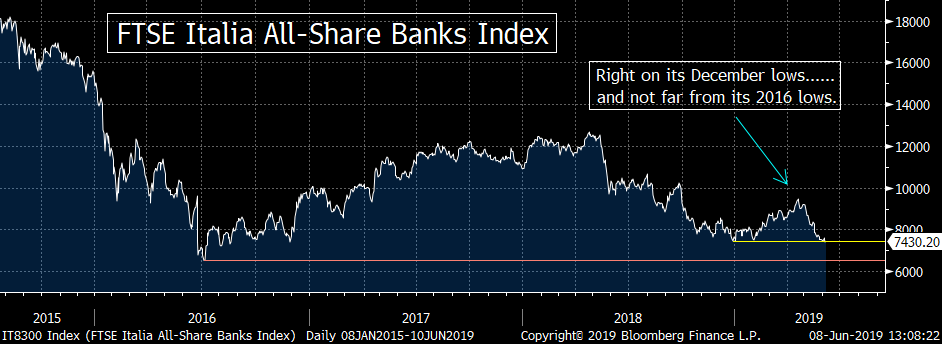

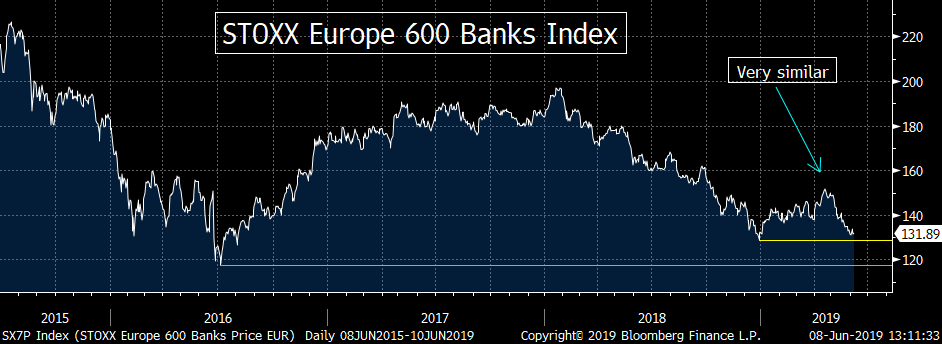

4) The action in the European banks is a big red flag for global markets.

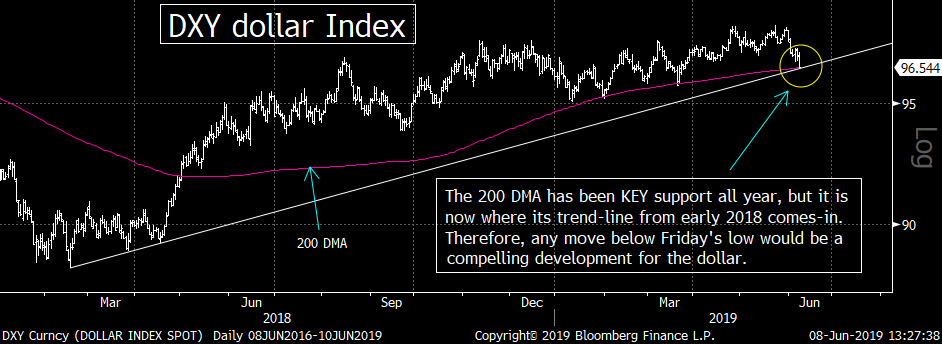

5) The DXY dollar index is testing TWO key support levels (at the same time).

6) Having said all this, the S&P is only 2.5% from its all time highs!

7) The S&P 500 index stands at a key technical juncture.

7a) Ditto for the Russell 2000.

8) Will a break-up of the tech stocks be positive? Doubtful over the short-term.

8a) Many big tech names have made "lower-highs" recently.

9) A technical look at gold.

10) A look at oil...What does the U.S./Saudi relationship under Trump mean?

11) Summary of our current stance.

Short Version:

1) Our call for a strong bounce in the stock market last weekend has worked out very well. A bounce in long-term interest rates helped early in the week, but the expectations of a Fed rate cut played an essential role as well (especially on Friday). However, we think the bounce was something that just worked off an oversold condition...and will not last much longer.

2) As much as the Fed talking in a more dovish fashion, they have not changed their actions to the degree they did in Dec/Jan, so we do not think it will have the same impact until they actually change their actions. More importantly, the reason for the 4th qtr decline was Fed...while this time around it's the trade war with China...and that situation does not look like it's going to change soon.

2a) Of course, some believe that since the Fed has told us they could/should be cutting rates soon, it has given investors the green light to buy stocks. However, the history of the last 10 years tells us that the Fed does not act until the markets have fallen a lot more than they have this time around. In other words, the Fed might indeed engage in a "pre-emptive" rate cut, but we believe it will be "pre-emptive" for the economy, not for the stock market (which tend to decline before the economy weakens considerably).

2b) In fact, we think it would be a dangerous precedent for the Fed to make a move after the kind of mild decline we've seen recently. Let's face it, 7%-10% pull-backs are normal and healthy. If the Fed reacts too soon, investors will throw all caution to the wind. That's what leads to bubbles…and given the level of leverage in the system today (especially in corp debt), it would be irresponsible to give investors that kind of over-confidence.

3) This does not mean that the Fed will not react soon. It just means that in our opinion, they won't act until or unless the stock market (& credit markets) experience more intense stress. That might take place quickly, so the Fed could still act quite soon...but those who buy now...instead of waiting for that decline...will get burned in our humble opinion.

3a) There are signs that much of the oversold condition has already been worked-off. The RSI chart has bounced back...and sentiment has bounced back as well. Also, the internals from Friday's rally were not very good...most of this rally has been led by defensive groups (just like the failed bounce that took place in mid-May).

4) Let's talk about one issue that few people are talking about...but has concerned us for some time. This is the European bank stocks. The group continues to act very poorly...and it European bank index has diverged considerably from the broad European stock indexes for over a year now....The European banks have not de-leverage themselves anywhere near to the degree that the U.S. banks have over the last decade, so this action is a big red flag for the global markets.

5) Maybe the biggest move last week came in the currency market…where the dollar saw a measurable pull-back. This took the DXY dollar index down to it VITALLY important support level (its 200 DMA and its trend-line from the 2018 lows (when this dollar rally began). Therefore, if it breaks below that line in any meaningful way over the coming days and weeks, it will be a compelling development on a technical basis. This, in turn, could/should have an important impact on several other asset classes (including emerging markets & commodities).

6) Ok, we've painted a pretty bleak picture so far, but there are certainly some reasons to be more constructive right now. First of all, the S&P is still only 2.5% below its all time highs!!! Also, it's a good bet to think that President Trump will not want to take the China trade issue to a level where it would do irreversible damage to the economy (in front of the 2020 election). However, we think he's more worried about 2020 than the summer of 2019. When you combine that with the Fed's "market dependency" and we think preparing for a further decline is a good idea.

7) The S&P 500 index is at a key technical juncture. It has formed an "ascending triangle" pattern, so the direction of the break out of that pattern will be key. The top line in this pattern is the Sept/April highs of 2940, so a break above that level would be quite bullish. However, we think the more important support level will be the March/June lows of 2720 (instead of the bottom line of the triangle pattern). Therefore, even though we remain quite cautious, we do believe investors need to be nimble...because if/when one of these lines is broken, it will lead to a much further move in the direction of the "break".

7a) The Russell 2000 is also at a key juncture. This important leading indicator has acted poorly recently...and it is trying to bounce-back into the sideways range it had been in from mid-Feb to mid-May. If it can regain that range, it will be constructive. If it fails...and rolls back over, it's going to be quite bearish. So this is another index whose next meaningful move should provide an important insight for the market over the rest of the summer.8 & 8a) Let's move to the all-important tech group. On the fundamental side, we question the contention made in some corners last week that anti-trust investigations will be positive for the group. Yes, it might be good over the long-term, but the "process" will not be a short one...so we're concerned about this issue over the short & intermediate-term. This is especially true given how so many key tech names made key "lower-highs" in April. If those are followed by "lower-lows", it will be Katie bar the door.

9) Gold is moving back on to many people's radar screens...and for good reason. It is testing it February highs, so a break above that level would be positive. However, as we've been saying for some time, it will take a rally above $1,380 (its highs from 2016) which would take it out of its multi-year sideways range. We must admit, however, that the yellow metal is getting over-bought on a near-term basis...so it could/should take a short-term "breather" soon. However, any meaningful break above $1,380 would confirm that the long-term trend in gold has changed to the upside.

10) What about crude oil? Well, instead of talking about its fundamental picture, we think it's also important to consider its political picture. President Trump has a strong relationship with the Saudi Crown Prince (and he shielded him after the murder of Jamal Khashoggi). The Saudis don't have the same influence they once did on crude’s price, but they're still the key player. President Trump doesn't want prices that are too high, but he doesn't want them too low (think jobs).....On the technical side of things, WTI is testing its 200 week MA. A break below that level would be bearish near-term, but we question some of the more bearish recent calls on the black gold.

11) Summary of our current stance.....Our calls have worked out quite well in recent weeks. We were cautious in late April...became more so after the trade negotiations broke down in early May...said the mid-May bounce would not hold...and called for a sharp bounce a week ago. This does not mean we'll be correct going forward, but we do worry that the uncertainties surrounding the trade war will be with us for a while. This, in turn, means economic growth and earnings growth estimates will continue to come down...which will not help the stock market. Also, even though the Fed has shifted to a more dovish stance, history tells us that they do not change their actions until the markets have fallen more than they have so far ("market dependent"). Therefore, we think the market will have to fall further to reprice itself to these new realities...and before the Fed will cut rates. With this in mind, we think the recent pop in the market is an opportunity to raise some cash...which can be used when a more compelling decline takes place......Finally, we'd just highlight that the dollar is testing KEY support...and thus any further decline could/should have a significant impact on some other asset classes (like emerging markets and commodities.)

Long Version:

1) Well, our call for a strong bounce in the stock market last weekend (and reiterated on Monday) worked out very, very well…as the major averages rallied between 3.9% and 4.7%! The main reasons for our cautious call (after staying cautious throughout May) were two fold. First, the stock market had become quite oversold…and over-hated…on a very-short-term basis. Therefore, stocks were ripe for a bounce…no matter what the catalyst might be. Second, we said the probable stimulant for a pop in stocks would be a bounce-back in long-term interest rates (on a very-near-term basis). That did indeed provide a bit of a catalyst from Tuesday thru Thursday (especially Tuesday), when long-term yields jumped…but as we all know by now, those rates came crashing back down on Friday after the employment report hit the news-tape…..Therefore, there is no question that expectations of a Fed rates cut sooner rather than later also played a very big role in last week’s stock market rally (and the biggest role by the end of the week)……Even before Friday’s employment data, the Fed was already shifting its rhetoric to a more dovish stance. Comments from Fed Chairman Powell and Vice Chair Clarida…as well as from several regional Fed Presidents…made comments that stated the Fed would do want was needed to keep the expansion going…and they might even make a “pre-emptive” move if it looked like the trade war was going to cause a more serious down-turn than it already has. These comments, in turn, helped several Wall Street strategists to become more bullish on the stock market…and when the weak employment report came out on Friday, the stock market took off……The question is, will this bounce from a very oversold condition continue…or will it be just like the one we saw in mid-May…that was simply a bounce that worked-off an oversold condition? We think it will most likely be the latter.

2) We just do not believe that last week’s developments are the kind of bullish developments that will lead to a strong rally over the summer. In fact, we still believe that it is more likely that the next “meaningful break” for the S&P 500 index will be one that takes-out the May lows…rather than one that moves significantly above its April highs. (The S&P could retest those highs…or break them by a very slight amount…but we do not believe this rally will last.)……Don’t get us wrong, we certainly understand the argument that says the Fed’s more dovish comments (its more recent “shift”) will lead to a strong rally. Just look what took place the last time they “pivoted”…back at the end of December and in early January. It caused the deep (-20%) correction to end quickly…and was followed by a dramatic 25% rally over the next 4 months. Thus, we can see why many experts believe that the “Fed put” is a alive and well…and thus the stock market will not fall any further from its early June lows……..As we said above, however, we do not shares this enthusiasm…for two main reasons. First, the number one reason that caused the deep correction during the 4th quarter was the Fed’s tightening cycle. (It took a while for it to have an impact on the stock market…like it always does…but it obviously DID finally had a negative impact.) However this time, it has been the administration’s trade policies that have had the biggest impact on the most recent decline. Even though the administration is going to hold-off on its threats against Mexico, it has become more and more evident that the trade war with China is going to be with us for a long time. Therefore, the issue that CAUSED the recent pull-back has NOT been erased yet…like it was back in early January…so we believe more downside movement is probable.

2a) The second reason why we believe the Fed’s rhetoric from early last week won’t have the same impact it did back at then is because last week’s move simply took the Fed from being “on the sidelines” and “patient”…to being more dovish in their rhetoric. However, they are STILL ON THE SIDELINES. Back in the late 4<sup>th</sup> quarter, the Fed went from stating that rates were “far from neutral”…and heavily involved in a tightening process…to one where they ended their tightening policies. This was a major change in what the Fed was actually doing!!! This time, the Fed has not shifted its actually policy yet…like they did in December/January!!!!........You now might be saying to yourself, “Hold on Maley, Friday’s employment report makes it MUCH more likely that the Fed will cut rates in July (and maybe even June), so we don’t have to wait until they actually shifts policy in order to buy, buy, buy!” This might indeed be true, but we do not think so. They Fed might indeed do a pre-emptive rate cut after Friday’s employment report. However, the history of the past 10 years (since central bank liquidity has become SO important to the direction of the markets)…shows that the Fed does not make their move until the markets fall further than they have so far this time around!!!!!! In other words, as we’ve been saying (and proving) for years now, the Fed is more “market dependent” than “data dependent” when they make decisions like these. Therefore, we believe they will not cut rates until the stock market has fallen further (and probably until we see deeper cracks in the credit markets)…….One only has to look at when they started programs like QE2, operations twist, QE3…or when they took a lengthy pause in early 2016 after their first rate hike. On each of those occasions, the Fed only made those accommodative moves AFTER the S&P had seen a percentage decline that fell into the mid-teens or more! We haven’t seen that yet…and until we do, we do not think the Fed will cut rates.

2b) Let’s face it, a decline of 7%-10% can happen at ANY TIME (even in the middle of fabulous advances). We don’t even need to see/hear any “new-news” to create them! Sometimes they only take place because the stock market has become over-bought and extended on a near-term basis. These kinds of declines are normal and healthy…and thus any move by the Fed to stem the tide after such a small decline would set a DANGEROUS PRECIDENT. It would convince investors that not only was the “Fed put” alive and well…but it was very much “in the money” AND CONSTANT. Why would investors have any need to be prudent if they thought that the Fed would step-in and save the day on ANY little decline??? It would be like the spoiled brat whose parents buy their way out of every little problem for their children. Eventually, it comes back to kick them in the teeth. In other words, an actual change in policy…after such a small decline in the markets and after only a slight weakening of the economy will only serve to simply cause another serious bubble. Therefore, it is our opinion that given how much leverage that exists in the system today (especially in the corporate debt market…which is becoming more and more obvious every day), the Fed would be irresponsible if they cut rates too early. Yes, we believe that although the “Fed put” IS still alive and well…but we believe it is further “out of the money” than most people think…and that we’ll see lower-lows in the stock market before the Fed plays Mighty Mouse and “comes to save the day”.

3) What we’re saying is that we do not believe the Fed will act “too early”, BUT this does not mean they won’t act soon. In other words, “too early” is not a phrase we’re using to highlight a “timing” situation. Instead, we believe it will be a “pricing” situation. If the stock market rolls over soon…and the credit markets see some bigger cracks (like they finally did in December of last year), the Fed will act quickly. The problem with this scenario is that investors who buy NOW…in anticipation of at Fed cut without a drop in prices…will get burned in our humble opinion……Once the stock market goes back to focusing on the trade war with China…and the uncertainties that will be with us for quite a while on this issue…earnings estimates will fall. (This is something we’ve been saying for a while now would take place…and we finally saw some of that last week. We should see that from other corners of Wall Street very soon…and if things continue to be uncertain, the original cuts we become deeper ones before long.) Therefore, once the oversold condition has been worked-off in the stock market, it should roll-back over quite quickly.

3a) There are already signs that the vast majority of the oversold condition has been worked off. The RSI charts have bounced nicely…bearishness has faded considerably (with the DSI data moving from 9% bulls for the Nasdaq on Monday of last week…to 55% by Friday)…..On top of this, the “internals” for the rally on Friday were not very good. Volume was very low (just 2.6bn shares) during the 1% rally…and breadth was quite mediocre for a day where the averages rallied more than 1%. (The breadth on the S&P 500 was just 3 to 1 positive…and it was just 2.5 to 1 positive for the NYSE Composite Index.) We also saw the rally fade a little big in the afternoon…and the S&P was unable to hold above its 50 DMA……We’d also note that much of last week’s rally was led by defensive groups (utilities, consumer staples)…just like May’s failed bounce was been led. So although it’s not out of the question that we could still go back and retest the April highs again…the economic data is slowing…earnings growth estimates are coming down…the stock market is no longer oversold…and the internals of last week’s rally were not all that impressive. Therefore, we think the stock market will roll-back over quite soon.

4) Let’s move to another issue that concerns us right now. While everybody has been (rightfully) talking about the trade war with China, Iran, Breixt, earnings, etc…few people (outside of ourselves) have been talking about the European banks. Not only did they have a very rough month during May, but the bounce they’ve seen over the past week (when many/most other global stock were rallying nicely) was absolutely feeble….The group is being led lower by the Italian bank stocks. They actually closed below their late December highs last week…and not too far from their 2012 European crisis lows. A lot of European banks (especially in France) own a lot of bank debt in Italy…so it’s no surprise that the STOXX Europe 600 Banks index was flat last week during the global rally. This European bank index stands only 2% above its December lows…vs. the broad STOXX Europe 600 index…which stands more than 14% above its own December lows! (That’s quite a disconnect. In fact, as the third chart below shows, they started diverging over a year ago…in May 2018.)…….As we have been saying ad nauseam for years, the European banks did not de-leverage themselves anywhere to the degree the U.S. banks have over the past decade. Therefore, the HORRIBLE action in this group is a BIG red flag for other markets around the globe.

5) Maybe the biggest move last week came in the currency market…where the dollar saw a measurable pull-back. This took the DXY dollar index down to it VITALLY important support level…its 200 day moving average (200 DMA). That line has provided ROCK SOLID support for the dollar all year this year…bouncing off of it in January, February and twice in March. However, the 200 DMA on the DXY is ALSO where the trend-line going all the way back to the early 2018 lows (when this dollar rally began). Therefore, if it breaks below that line in any meaningful way over the coming days and weeks, it will be a compelling development on a technical basis…..Having said this, we’d have to see a drop below its March lows of 96.00…and probably below its January lows near 95…before we’d say that the almost 6-month trend for the green back has reversed, BUT any further decline in the dollar would still be important for the currency markets………Well, what would this all mean? It’s hard to speculate what it will mean for U.S. stocks, but we DO have to point out that no matter what it would mean theoretically for the U.S. stock market, there are many, many, many examples in history where a falling dollar has coincided with a rising stock market…but just as many examples where they have fallen in tandem over time. Therefore, it’s not as easy to predict what kind of impact it will have this time around. On Friday, the decline simply meant that rates were probably headed lower…and thus stocks were rally…but one day does not make a correlation…..…..HOWEVER, it should have an important impact on some other asset classes…like the emerging markets and commodities…which have a stronger correlation with the dollar than the U.S. stock market. We’ll have more on in later points, but we just want to point out that the DXY is testing a key support level. Thus how is acts next week (and the weeks that follow) should be very important…no matter how it impact U.S. stocks.

6) Ok, we’ve painted a pretty bleak picture so far. Given that the S&P 500 Index is only 2.5% below its all-time highs…and still stands 22% above its December lows…maybe we’ve painted a picture that is too bleak! We don’t mean to do this. First of all, even if we’re correct about the Fed…and they’ll wait before cutting rates…there are certainly indications that the Fed will still indeed step to the plate if needed at some point. That is a far cry from what they were saying after we were one-month into a pull-back during 4<sup>th</sup> quarter of last year. Back then (in early November), the Fed remained VERY hawkish in their verbiage…...Second of all, even though President Trump is playing hard ball with everybody right now, he needs the stock market to be rising and the economy to be improving in 2020 if he wants to get re-elected. Therefore, there are plenty of reasons to think that President Trumps words and actions will be much more conducive to a stock market rally as we’re moving through the 4<sup>th</sup> quarter of this year (and all of next year)…..As we’ve been saying for the past few weeks, the Trump administration won’t care as much about the stock market over the summer of 2019…as they will in 2020 (not even close)……..This is why we believe it is imperative for investors to work on contingency plans IN ADVANCE. If we do get another leg lower in the stock market this summer and/or early fall, you want to have a plan set up in advance to take advantage of this decline. Raise cash on rallies and make sure you know what you want to buy and at what levels you want to buy them (don’t try to buy them all at once…or at one level). Of course, you can adjust those plans as we move forward. However, as we learning in December, those with a plan in advance are the ones who “keep their heads when others around them are losing theirs” during sharp decline…and can take advantage of a situation where the baby is being thrown out with the bathwater. Those who are not prepared in advance (and don’t have any cash on hand) tend to get caught up in the moment…and sell at exactly the wrong time…instead of buying at great prices.

7) As much as we believe that the stock market will roll-back over soon, we HAVE to consider a much more bullish scenario…because the S&P 500 Index is at a key technical juncture. It has formed an “ascending triangle” pattern. Therefore, whichever way it breaks out of this pattern should be quite important for the intermediate-term potential for the stock market. If it breaks above its “double-top” level of 2940 in any meaningful way, it’s going to be VERY bullish on a technical basis. If, however, it rolls back over and breaks below the lower line of this pattern, it’s going to be bearish. (And if it breaks materially below its June 3<sup>rd</sup> lows, it’s going to be quite bearish for how the market acts over the rest of the summer.) In other words, the action in the stock market over the month of June should be incredibly important as to how it acts over the rest of the summer. Therefore, even though we are quite cautious on the stock market right now, it will be vitally important to stay nimble. Just because the fundamental back-drop is not conducive to a strong rally from here does not mean we won’t get one…and the technical picture is telling us that a rally is possible (even if we think it is less than likely)……..In the end, the most important thing we’ll be watching is the old highs (from last September and this April…at 2940)…and the lows from March & June (at 2720). Any meaningful break of either of those levels should create a significant FURTHER move in the direction of that “break”.

7a) Staying on the technical side of things, one of the reasons we continue to stay cautious on the stock market is the action in the Russell 2000. Despite the fact that the trade war with China should having less of an impact on companies whose profits are domestically generated, this small cap index has acted very poorly in recent months. As we all know, this group topped-out before the rest of the market in 2018, so this action continues to be a big yellow warning flag for the rest of the stock market…….The Russell has broken below its trend-line from December…has stayed below its 200 DMA…and it recently fell below its 3+ month sideways range. Last week’s bounce took it back up to the bottom of that range, so if it can rally further, it will give some relief to the rest of the market. However, it will have to rally back above its 200 DMA…AND above its sideways range (above 1600) in a meaningful way…before we’d be able to say that this index was going to help the broad market in any way. (In fact, it would take a rally above its all-time highs to raise a big green flag on the small cap sector.)……..In other words, the small cap stocks remain a key headwind for a stock market that has actually done nothing for 16 months.

8) Let’s move to the all-important tech stock group…..You’ve all been inundated with opinions about what kind of impact the potential anti-trust investigations might have…and what kind of regulations might come out of them…so we won’t bore you by adding to those opinions. Instead, we’d just like to address the growing belief that further regulations or a breaking up of some of these companies will actually be positive for the group. Yes, these potential investigations could force these big tech companies to change their behavior in a positive fashion. Also, a break-up of any of these companies could actually enrich investors (just like the breaking-up of Standard Oil did a couple of generations ago)…..However, this reminds us of the argument that many put forth when the first calls for the impeachment of President Trump became public over a year ago. Some people said that the impeachment of Trump would actually be bullish for the markets…because VP Pence would go forward on many of Trump’s pro-business policies, but without all the damaging rhetoric. However, as we said at the time, the “process” of impeaching the President would take a long time…and would be quite damaging. It would push-out any pro-business plans well into the future…and actually hurt the economy & the markets. So even if getting rid of the President was bullish on a long-term basis (the way some people argued), it would be bearish over the intermediate term (for many, many months…if not years)……We believe that it is important to consider that the same could/should be true for these big tech companies. It might be bullish over the very long-term, BUT they’d have to spend a lot of time and resources dealing with the legal battles…that it’s hard to think it would be bullish over the intermediate term…and investors should act accordingly.

8a) This is particularly true given that the charts in many of these names look pretty dicey. Actually, on a very-short-term basis, all of the FAANG stocks had become quite oversold, so it’s no surprise that they all bounced late last week. They could all easily see further advances on a short-term basis. However, those bounces had better be strong…and last a long time…because all of them (except for GOOGL) experienced significantly “lower-highs” back in April. In fact, this is true of several key tech companies away from the FAANG names (like NVDA, MU and WDC)…..Of course, there were plenty of tech stocks that had been working very well all year this year, so we are certainly not trying to say that we’re about to see a repeat of 2000-2003. We also don’t think these high flying names will get clobbered to the same degree they did back in the 4<sup>th</sup> quarter. (Back then, they were wildly “over-owned” by many/most institutional investors…and not just hedge funds. So those over-weighted positions will not have to be unwound to the same degree they were last year.) However, if these names cannot see much upside follow-through after last week’s bounces, it’s still going to raise some concerns. In other words, if these stocks follow their “lower-highs” from April…with “lower-lows”, it’s going to be very bearish for these names…..Of course, any “lower-lows” would entail a move below their December lows…and none of these stocks is anywhere near to testing those levels. Therefore, we don’t want to overstate this scenario, but there’s no question that the tech group faces the kind of head winds…on both the fundamental and technical side of things…tha

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22